Free Cash Flow Yield: The One Metric That Separates Real Wealth Creators from Accounting Illusions in Indian Markets — A Complete Guide for Value Investors

Interest Coverage Ratio: The Debt Survival Metric That Reveals Whether Indian Companies Can Pay Their Lenders — Or Are Heading Toward Financial Disaster

March 31, 2026

DuPont Analysis: The X-Ray Machine That Reveals the TRUE Quality of ROE — Why High Return on Equity Can Be Dangerous and How Smart Indian Investors Decode It to Find Genuine Multibaggers

April 1, 2026

📅 Published: 1 April 2026 — Morning Edition | By Manish Goel, SEBI Registered Research Analyst (INH100004775)

📲 Join our Telegram channel @longtermequityy for daily value investing insights

Why Earnings Lie But Cash Never Does — The Case for Free Cash Flow Yield

In the Indian stock market, thousands of retail investors rely on the Price-to-Earnings (PE) ratio to decide whether a stock is cheap or expensive. While PE has its place, it is dangerously incomplete. Earnings — the “E” in PE — can be manipulated through accounting adjustments, changed depreciation policies, one-time gains, inventory revaluations, and aggressive revenue recognition. The number that appears on the profit-and-loss statement is, in many cases, an opinion dressed up as a fact.

Free Cash Flow (FCF), on the other hand, is the cold hard truth. It represents the actual cash a business generates after paying for its operations and reinvesting in its future through capital expenditure. You cannot fake cash. It is either in the bank or it is not. And when you express FCF as a percentage of a company’s market capitalisation, you get the Free Cash Flow Yield (FCF Yield) — arguably the single most powerful valuation metric available to value investors in India today.

What Is Free Cash Flow Yield? The Formula Explained

The formula is elegantly simple:

Free Cash Flow Yield = (Free Cash Flow ÷ Market Capitalisation) × 100

Where: Free Cash Flow = Cash from Operations − Capital Expenditure

For example, if a company generates ₹12 crore in free cash flow and its market capitalisation is ₹1,983 crore, its FCF Yield is approximately 0.60%. But if a smaller company generates ₹50 crore in FCF with a market cap of ₹500 crore, its FCF yield would be a stunning 10% — meaning for every ₹100 you invest, the business is generating ₹10 of real, distributable cash every year.

Why FCF Yield Is Superior to the PE Ratio

The PE ratio relies on reported net profit, which can be inflated or deflated by non-cash items like depreciation, amortisation, deferred tax assets, exceptional items, and changes in working capital. Indian companies — particularly in the mid-cap and small-cap space — are notorious for window-dressing their earnings to attract investors during bull markets.

FCF Yield cuts through this noise entirely. Consider these critical advantages:

1. Cash Cannot Be Faked: While profits are an accounting construct, free cash flow is verified through bank statements and auditor confirmations. A company reporting ₹100 crore in profit but only ₹20 crore in operating cash flow is flashing a massive red flag — the earnings quality is poor, and the “profits” may exist only on paper.

2. It Accounts for Reinvestment Needs: Some businesses look profitable but consume enormous amounts of capital just to maintain their current operations. A steel plant might report healthy profits but require ₹500 crore in annual capex for maintenance. FCF Yield captures this reality — high-capex businesses will show lower FCF yields, correctly signalling that less cash is available for shareholders.

3. It Reveals True Shareholder Value: Free cash flow is what ultimately funds dividends, buybacks, debt reduction, and organic growth. A company with a high FCF yield has multiple options to reward shareholders, while a company with a low FCF yield — regardless of its PE ratio — may struggle to deliver real returns.

4. It Works Across Sectors: Unlike PE ratios which vary dramatically by industry, FCF Yield provides a more standardised comparison across sectors because it measures the same thing everywhere — how much real cash does the business produce per rupee of market value?

How to Interpret FCF Yield: Benchmarks for Indian Markets

While there is no universal “correct” FCF Yield, here are practical benchmarks Indian investors can use as a starting framework:

FCF Yield above 8%: Potentially undervalued — the market may be underappreciating the company’s cash generation ability. This is the sweet spot for deep value investors.

FCF Yield between 4% and 8%: Fairly valued to moderately attractive — the company is generating decent cash relative to its valuation. Good for quality-at-reasonable-price (QARP) investors.

FCF Yield between 1% and 4%: The market is pricing in significant future growth. The company needs to deliver on growth expectations to justify its valuation.

FCF Yield below 1%: Either the company is in a heavy investment phase (which may be justified for growth companies) or the stock is significantly overvalued relative to its cash generation ability.

The Five Red Flags FCF Yield Exposes Instantly

Red Flag #1 — The Profit-Cash Divergence: When a company consistently reports rising profits but flat or declining free cash flow, it usually means earnings quality is deteriorating. This divergence has preceded major stock collapses in Indian markets — from Satyam to more recent mid-cap blowups.

Red Flag #2 — Negative FCF Despite Profitability: A company showing profits but generating negative free cash flow is essentially telling you that its operations are consuming more cash than they produce. This is particularly dangerous in capital-intensive businesses where investors may be lulled by “strong” profit numbers.

Red Flag #3 — Declining FCF Yield Over Time: If a company’s FCF Yield has been declining over three to five years while its stock price has been rising, it means the market’s expectations are running far ahead of the company’s actual cash generation improvement. This is a classic setup for a mean-reversion correction.

Red Flag #4 — FCF Yield Far Below Earnings Yield: The earnings yield is simply the inverse of the PE ratio (1/PE). If a company’s FCF Yield is dramatically lower than its earnings yield, it means a large portion of reported earnings are not being converted into cash — a clear sign of poor earnings quality.

Red Flag #5 — High Debt + Low FCF Yield: Companies with significant debt obligations and low FCF Yield face a double threat — they may not generate enough cash to service their debt while simultaneously growing the business. This combination has destroyed wealth for countless Indian investors.

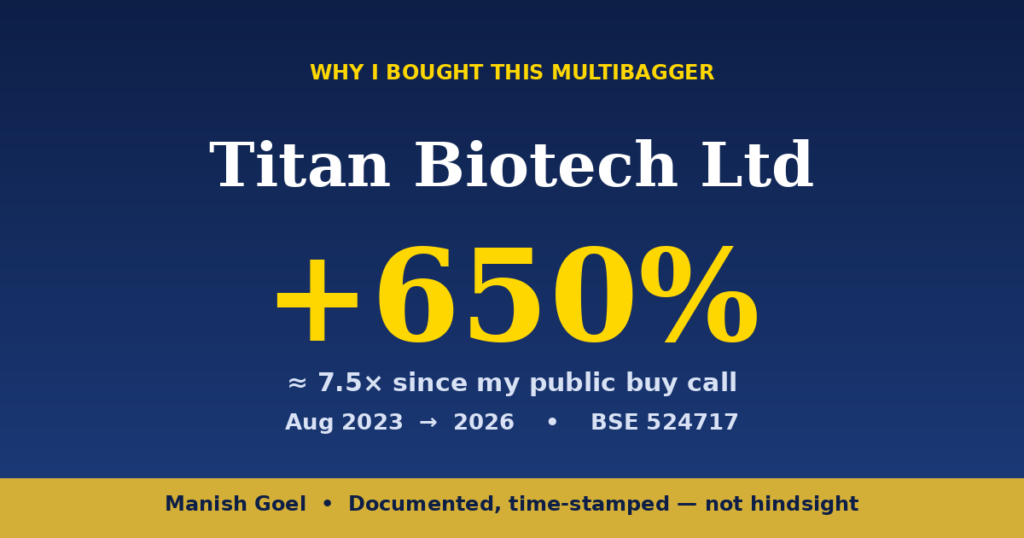

Case Study: Titan Biotech Ltd — A Quality Compounder with Strong Cash Flows

Let us examine how FCF Yield analysis applies to a real Indian company. Titan Biotech Ltd (BSE: 524717), a leader in biotechnology products and life sciences ingredients, provides an excellent illustration of quality cash flow characteristics:

Key Financials (FY2025):

📊 Market Cap: ₹1,983 Crore | Stock Price: ~₹480

📊 Sales: ₹156 Crore | Net Profit: ₹22 Crore

📊 Operating Cash Flow: ₹20 Crore | Free Cash Flow: ₹12 Crore

📊 ROCE: 16.9% | ROE: 15.0%

📊 Debt: ₹3 Crore (Virtually Debt-Free)

📊 Promoter Holding: 55.78% | 5-Year Profit CAGR: 26%

📊 FCF Yield: ~0.60%

At first glance, Titan Biotech’s FCF Yield of approximately 0.60% might seem low. However, context is everything in value investing. The company is in a high-growth reinvestment phase — with 5-year sales CAGR of 15% and profit CAGR of 26%, the market is correctly pricing in significant future growth potential. The company’s near-zero debt (₹3 crore against ₹175 crore in total assets) means virtually all of its cash generation is available for growth reinvestment rather than debt servicing.

What makes Titan Biotech particularly interesting from an FCF perspective is the quality of its cash conversion. With operating cash flow of ₹20 crore against net profit of ₹22 crore, the company converts approximately 91% of its profits into operating cash — an exceptional ratio that indicates high earnings quality. Many Indian companies, especially in the small-cap space, struggle to convert even 50-60% of their profits into cash.

As Titan Biotech’s growth phase matures and capital expenditure normalises, its FCF Yield should expand significantly — creating a powerful dual engine of returns from both business value growth and improving cash distribution potential.

Building an FCF Yield-Based Investment Framework

Here is a practical step-by-step framework for incorporating FCF Yield into your Indian stock analysis:

Step 1 — Calculate Trailing FCF Yield: Take the last four quarters of operating cash flow, subtract capital expenditure, and divide by the current market capitalisation. Use screener.in or Trendlyne to access cash flow statements easily.

Step 2 — Examine the 5-Year FCF Trend: A single year’s FCF can be misleading due to lumpy capex or working capital swings. Look at the five-year trend. Companies that consistently generate positive and growing FCF are far more reliable wealth compounders.

Step 3 — Compare FCF Yield to Earnings Yield: If FCF Yield is close to or higher than earnings yield (1/PE), it indicates excellent earnings quality. If FCF Yield is significantly lower, investigate why — the gap might reveal aggressive accounting or heavy reinvestment needs.

Step 4 — Sector-Adjust Your Expectations: Capital-light businesses like IT services, FMCG, and pharma should generally show higher FCF yields than capital-heavy businesses like metals, infrastructure, and real estate. Compare FCF Yield within the same sector for the most meaningful insights.

Step 5 — Look for the “FCF Inflection”: The most profitable investments often come from identifying companies about to transition from heavy investment (low FCF) to harvest mode (high FCF). This inflection point is where the FCF Yield starts expanding rapidly, and the market begins to re-rate the stock higher.

Common Mistakes Indian Investors Make with FCF Analysis

Mistake #1 — Ignoring Growth Capex vs. Maintenance Capex: Not all capital expenditure is equal. Growth capex (building new capacity) creates future value, while maintenance capex (replacing old equipment) merely preserves current capacity. When analysing FCF, try to distinguish between the two. A company spending heavily on growth capex may have a temporarily low FCF Yield but could be building massive future earning power.

Mistake #2 — Using Only One Year’s Data: FCF can swing wildly year-to-year due to working capital changes, lumpy capex cycles, or one-time payments. Always use a three-to-five-year average FCF for a more reliable yield calculation.

Mistake #3 — Comparing Across Different Growth Stages: A mature, slow-growing business should have a higher FCF Yield than a fast-growing company reinvesting aggressively. Comparing the two directly without adjusting for growth would lead you to always prefer mature businesses and miss the next multibagger.

Mistake #4 — Ignoring Working Capital in FCF: Some businesses show strong operating profits but terrible free cash flow because their working capital keeps expanding — receivables grow, inventory builds up, and cash gets trapped in the business cycle. Always check whether FCF is being suppressed by poor working capital management rather than legitimate growth investment.

The Bottom Line: Let Cash Be Your Guide

In the famous words often attributed to investing legends: “Revenue is vanity, profit is sanity, but cash flow is reality.” In Indian markets, where accounting creativity can sometimes rival Bollywood storytelling, free cash flow yield gives you the unvarnished truth about a company’s financial health and valuation.

The next time you evaluate a stock, before looking at the PE ratio, before checking the EPS growth, before reading the management commentary — check the Free Cash Flow Yield first. It will tell you more about the company’s true value and quality than almost any other single metric. Combined with other fundamental indicators like ROCE, debt levels, and promoter holding patterns, FCF Yield gives you a powerful, manipulation-resistant framework for identifying genuine wealth creators in India’s exciting but often treacherous equity markets.

⚠️ Disclaimer: Manish Goel is a SEBI Registered Research Analyst (INH100004775). Multibagger Securities is a SEBI Registered Investment Adviser (INA100007736). This article is for educational purposes only and does not constitute a buy, sell, or hold recommendation for any security. Investors must conduct their own due diligence or consult a SEBI-registered advisor before making any investment decisions. Past performance does not guarantee future results. Stock market investments are subject to market risks.

📲 Join our Telegram channel @longtermequityy for daily value investing education and analysis.

{kind=link}

{kind=link}

{kind=link}