Why Promoter Confidence Is the Ultimate Quality Signal

The Compounding Machine: How Quality Stocks

March 20, 2026

The ROCE Secret: Why This One Metric Separates Wealth Creators from Wealth Destroyers

March 21, 2026

March 20, 2026

(Friday)

In the world of value investing, we often spend enormous time analysing balance sheets, income statements, and cash flow trends. Yet one of the most powerful — and most overlooked — signals of long-term business quality is deceptively simple: what are the promoters doing with their own money?

Promoter confidence is not a secondary metric. It is arguably the single most important qualitative indicator of a company’s future. When those who know the business best — its founders, its family promoters, its largest insiders — continue to hold, increase, or pledge minimal shares, the message to the discerning investor is clear: they believe deeply in the long-term compounding potential of their own enterprise.

The Promoter Confidence Framework

Before we dive into specifics, let us understand what promoter confidence actually means in practical terms. In the Indian equity markets, promoters are typically founders, their families, or institutional entities that built and continue to run the company. They sit at the top of the information pyramid. They know the order book, the pipeline, the competitive threats, the regulatory environment — everything that is not yet reflected in public disclosures.

When promoters maintain or increase their stake in a company — especially during periods of broader market weakness — they are making an implicit statement: “At current prices, the market has not yet understood the true value of what we have built.” This is the most powerful vote of confidence any investor can receive.

Conversely, promoters who consistently reduce their stake, pledge shares heavily, or show erratic ownership patterns are often signalling internal concerns — concerns that retail investors will only understand months or years later, when it is already too late.

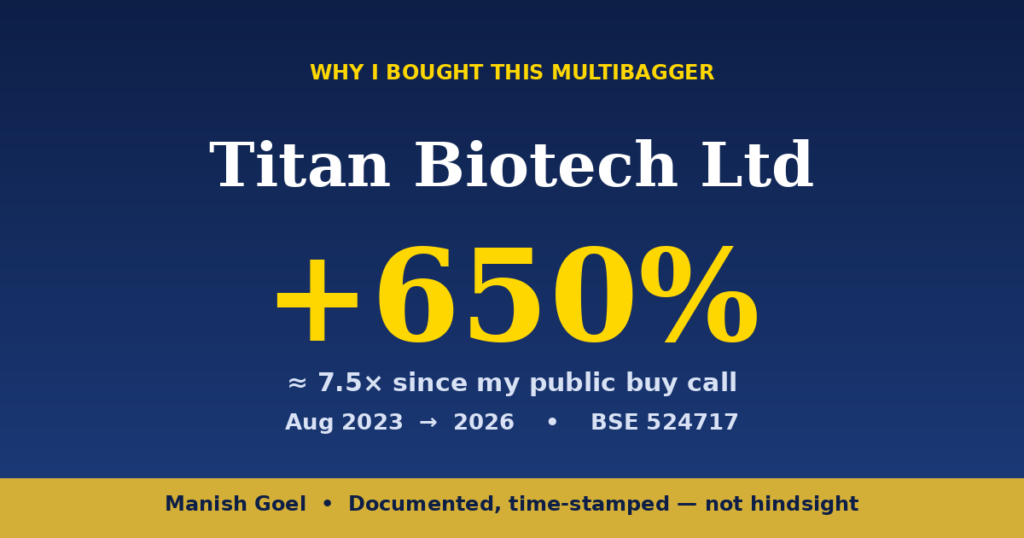

Titan Biotech: A Case Study in Promoter Conviction

Titan Biotech Ltd (BSE: 524717) is a compelling illustration of how promoter conviction, combined with genuine business quality, creates extraordinary long-term wealth for patient investors. The company — engaged in the manufacture and export of microbiological culture media, dehydrated culture media, and biochemical diagnostic reagents — has built a formidable competitive position over decades of focused execution.

What stands out about Titan Biotech is not just the impressive revenue trajectory from approximately ₹60 crore to over ₹300 crore. What stands out is the character of that growth. It has been consistent, margin-expanding, and built on a foundation of genuine scientific capability and customer trust. These are precisely the conditions under which promoters develop and maintain deep conviction in their enterprise.

The management team at Titan Biotech has demonstrated through their actions — not merely their words — that they view the company as a long-term compounding machine, not a short-term financial engineering exercise. The company remains essentially debt-free, a decision that reflects management’s preference for organic, sustainable growth over leveraged expansion. Promoters who run debt-free companies tend to have longer time horizons and stronger alignment with minority shareholders.

Why Quality Businesses Always Trade at a Premium

One of the most common mistakes retail investors make is equating “expensive” with “overvalued.” This conflation has cost many investors the opportunity of a lifetime. High-quality businesses — those with consistent profitability, expanding margins, strong ROCE, debt-free balance sheets, and confident promoters — almost always trade at premium valuations. And they deserve to.

Think about it this way: if you found a business that could compound your capital at 20-25% per year for a decade, would you pay a slight premium for that? Of course you would. The entire principle of compounding rests on the idea that future value is worth a great deal more than what meets the eye today. Stocks like Titan Biotech that have delivered 50x returns (from approximately ₹8 to ₹400) were rarely “cheap” at any point in their journey. Yet patient investors who recognised the quality never needed to wait for a “bargain entry.”

Cheap stocks, on the other hand, are often cheap for good reason. Low promoter holding, high debt, shrinking margins, inconsistent earnings — these are the hallmarks of value traps that seem attractive on paper but destroy capital over time. The discipline of a quality investor is to resist the siren call of “cheap” and instead focus on the compounding power of quality.

The Biotech Sector: A Tailwind for Long-Term Compounders

Promoter confidence in Titan Biotech does not exist in a vacuum. It is reinforced by the macro tailwinds of India’s rapidly growing biotechnology and life sciences sector. India’s biotech industry has been growing at over 15% annually, fuelled by domestic healthcare demand, export opportunities, and significant government policy support. The COVID-19 pandemic underscored the strategic importance of indigenous biotech capability, and capital — both public and private — has been flowing toward companies with proven track records.

Titan Biotech sits at an interesting intersection: it is not a speculative biotech startup burning cash in pursuit of an uncertain drug approval. It is a proven, cash-generative, export-oriented manufacturer of essential diagnostic and research inputs. This is a fundamentally different risk profile — one that justifies higher confidence from promoters who have seen the business cycle through multiple macro environments.

The global diagnostics market — a key addressable market for Titan Biotech’s products — is expanding rapidly, driven by ageing populations worldwide, the rise of lifestyle diseases, and increased healthcare spending in emerging markets. India’s scientific research infrastructure is also scaling significantly, with more universities, research institutions, and pharmaceutical companies requiring the kind of high-quality culture media and reagents that Titan Biotech manufactures. These structural tailwinds do not reverse easily, and promoters who have built their business to serve this growing demand have every reason to maintain their conviction.

The Buffett-Munger Framework Applied: Know What You Own

Charlie Munger famously said: “Show me the incentive and I’ll show you the outcome.” In investing, the promoter’s incentive structure is among the most important variables to understand. When a promoter’s personal wealth is concentrated in the stock they manage, they have a powerful incentive to ensure the business delivers. They are not hired managers with stock options that vest in three years — they are owners whose family legacy is tied to the enterprise.

Warren Buffett has always emphasised the importance of understanding management character and capability as prerequisites for investment. A business can have excellent economics, but if the people running it are not trustworthy or lack the vision to compound capital effectively, the economics will eventually be squandered. Conversely, exceptional management can often navigate a challenging environment and emerge stronger.

In this framework, promoter confidence becomes a proxy for management quality. Promoters who hold their shares through market cycles, who avoid excessive dilution, who maintain conservative balance sheets, and who demonstrate consistent execution — these are the hallmarks of the rare individuals worth entrusting your capital to for a decade or more.

Patience: The Rarest and Most Valuable Investment Quality

The journey from ₹8 to ₹400 in Titan Biotech’s stock price was not a straight line. There were periods of consolidation, periods of broader market panic, periods where the stock appeared to go nowhere for months. Investors who lacked patience — who sold during drawdowns or switched to “more interesting” opportunities — missed most of the compounding journey.

This is perhaps the most profound lesson that promoter confidence teaches us: the promoters did not sell. Through market cycles, through sectoral headwinds, through periods of uncertainty, they maintained their conviction because they understood what they had built. The retail investor who mirrors this patience — who buys quality and holds through volatility — is essentially co-owning the business alongside the people who know it best.

As Philip Fisher wrote in Common Stocks and Uncommon Profits: “The stock market is filled with individuals who know the price of everything, but the value of nothing.” The investor who understands the value of promoter confidence — and is willing to hold patiently alongside high-conviction promoters — is in a rare and privileged position.

Building a Coffee Can Portfolio Around Promoter Confidence

The Coffee Can Portfolio approach — conceptualised by Robert Kirby and popularised in India by Saurabh Mukherjea — involves buying quality businesses and holding them for a decade or more without trading. The entire philosophy rests on identifying companies where promoter conviction, business quality, and sector tailwinds align to create durable compounders.

The screening criteria for a Coffee Can Portfolio naturally filters toward high promoter confidence. You want companies with consistent revenue and profit growth, high ROCE (typically above 15%), minimal or no debt, and management that has demonstrated the ability to allocate capital intelligently over long periods. Titan Biotech, with its revenue trajectory from ₹60 crore to ₹300+ crore, expanding margins, and debt-free balance sheet, exemplifies the kind of company that belongs in this category.

Building wealth through such a portfolio is not about finding the next short-term trade or catching a sector rotation. It is about identifying businesses where the promoters themselves are your most important co-investors — and trusting that their long-term conviction, backed by intimate knowledge of the business, will ultimately be proven correct.

The Investment Takeaway

The next time you evaluate a stock, go beyond the P/E ratio and the EPS growth numbers. Ask yourself: what are the promoters doing? Are they holding? Are they buying? Are they pledging minimal shares and running a clean, debt-free operation? Are they building for the next decade or extracting value for themselves at the expense of minority shareholders?

Promoter confidence is not a guarantee of returns. No single metric is. But as part of a holistic quality investing framework — one that looks at business economics, competitive moats, sectoral tailwinds, and management character — it is an invaluable signal. The businesses that have created the most long-term wealth in India have almost invariably been those where promoters believed deeply in what they built and allowed compounding to do its patient, powerful work.

Quality businesses, led by confident, trustworthy promoters, operating in growing sectors — this is the formula. It is not complicated. It just requires patience and the discipline to focus on what matters most.

Disclaimer: This article is for educational purposes only. The information provided does not constitute investment advice. Consult your financial advisor before making any investment decisions. Multibagger Securities Research & Advisory Pvt. Ltd. (INA100007736) is a SEBI Registered Investment Advisor.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}