SME IPO Traps: 7 Deadly Red Flags Every Indian Investor Must Know Before Applying — Why 90% of SME IPOs Destroy Wealth and How to Protect Your Capital

Holding Company Discount in India: How Smart Investors Find Hidden Value in Parent Companies — A Complete Guide for Indian Value Investors

March 27, 2026

The Gordon Growth Model: How to Calculate the True Intrinsic Value of Dividend-Paying Stocks — A Complete Valuation Guide for Indian Investors

March 27, 2026

March 27, 2026

(Thursday)

The SME IPO Frenzy That’s Burning Indian Retail Investors

India is in the grip of an unprecedented SME IPO boom. In the last two years alone, hundreds of small and medium enterprises have listed on the BSE SME and NSE Emerge platforms, raising thousands of crores from eager retail investors. The allure is irresistible — stories of 200-500% listing gains spread like wildfire on social media, WhatsApp groups buzz with “next multibagger IPO” tips, and FOMO (Fear of Missing Out) drives millions to apply blindly.

But here’s the harsh reality that nobody talks about: the majority of SME IPOs have destroyed wealth for retail investors. A study of SME IPOs listed between 2023 and 2025 reveals that over 60% of them are trading below their listing price within 6 months. Many have crashed 50-80% from their highs, wiping out the life savings of unsuspecting investors.

This is eerily similar to the F&O gambling epidemic. According to SEBI’s landmark September 2024 study, 93% of individual F&O traders incurred losses between FY22-FY24, with aggregate losses exceeding ₹1.8 lakh crores. SME IPOs are becoming the new wealth destruction machine for retail investors who don’t do their homework.

Today, with the Sensex at approximately 75,273 and the Nifty at 23,306 (as of March 25, 2026), let’s dissect the 7 deadly red flags that separate genuine SME opportunities from outright traps — and learn how to protect your hard-earned capital.

Red Flag #1: Artificially Inflated Pre-IPO Financials

This is the most dangerous and widespread trap in SME IPOs. Unlike mainboard IPOs that undergo rigorous scrutiny from top-tier investment banks and auditing firms, SME IPOs often have minimal institutional oversight. Many promoters engage in what’s called “window dressing” — artificially inflating revenues and profits in the 2-3 years before the IPO to make the company look like a high-growth story.

How do they do it? Common tactics include circular trading with related parties (Company A sells to Company B, which sells back to Company A through intermediaries), channel stuffing (pushing excess inventory to distributors to book revenue), capitalizing expenses instead of writing them off, and recognizing revenue prematurely before delivery or service completion.

How to spot it: Compare the company’s revenue growth rate in the 3 years before the IPO with the industry average. If a small company is growing at 40-50% while the industry grows at 10-15%, ask yourself — where is this extraordinary growth coming from? Check the cash flow statement. If profits are high but operating cash flow is negative or much lower than reported profit, the earnings may not be real.

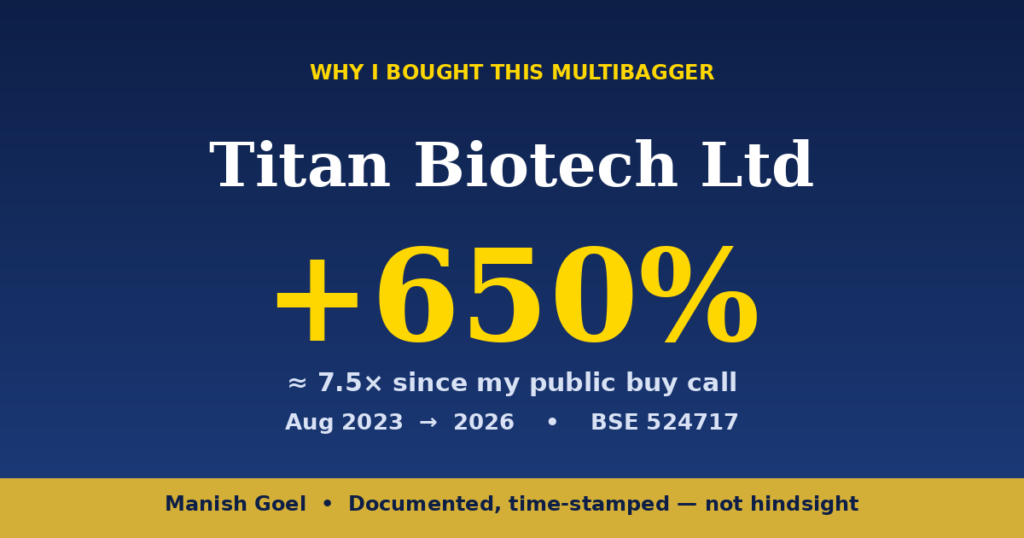

Compare this with a genuinely high-quality company like Titan Biotech Ltd (BSE: 524717), currently trading around ₹369. Titan Biotech’s growth has been organic, backed by real cash flows, zero debt, and consistent profitability over decades — not manufactured numbers designed to sell shares to unsuspecting investors.

Red Flag #2: Astronomical Valuations with No Track Record

Here’s a pattern that should alarm every investor: an SME company with ₹15-20 crore revenue and ₹2-3 crore profit comes to market at a valuation of ₹300-500 crores, implying a P/E ratio of 100-150x. By comparison, well-established large-cap companies with decades of proven track records trade at 25-40x earnings.

The logic promoters use is seductive: “We’re a high-growth company in a sunrise sector.” But growth without profitability, scale, or competitive advantage is just a story — and stories don’t generate returns, fundamentals do.

The valuation test: Before applying to any SME IPO, calculate the Price-to-Earnings ratio based on the IPO price and the last 12 months’ net profit. If the P/E is above 40x for a company with less than ₹50 crore revenue and no unique competitive moat, you’re likely overpaying. Also check the Price-to-Book ratio — if it’s above 8-10x for a manufacturing or trading company, the valuation is stretched.

Red Flag #3: Promoter’s True Intentions — The “Offer for Sale” Trap

Pay very close attention to the IPO structure. Every IPO has two components: Fresh Issue (new shares issued by the company to raise capital for business growth) and Offer for Sale (OFS) (existing shares sold by promoters or early investors to cash out).

When the OFS component is 50% or more of the total IPO size, it’s a massive red flag. It means the promoter is using the IPO primarily to sell their own shares and pocket the money — not to grow the business. Ask yourself: if the promoter believes the company has huge growth potential, why are they selling their shares to you at what they claim is still a “cheap” price?

What to look for: Ideal SME IPOs should have 70-100% fresh issue component, with the money earmarked for clear, specific business expansion (new plant, working capital, debt repayment). Be especially wary when the “Objects of the Issue” section in the prospectus lists vague purposes like “general corporate purposes” or “unidentified acquisitions.”

Red Flag #4: The Grey Market Premium (GMP) Illusion

Perhaps the most destructive phenomenon in Indian SME IPOs is the blind reliance on Grey Market Premium (GMP). GMP is the unofficial premium at which IPO shares trade in the grey market before listing. Investors see a GMP of ₹200-300 and assume they’ll make guaranteed profits on listing day.

Here’s what most investors don’t know: GMP can be easily manipulated. Promoters and their associates can create artificial demand in the grey market by placing buy orders through intermediaries. This drives up the GMP, which in turn drives more retail applications (since people see high GMP and assume it’s a “sure shot”), which leads to higher subscription numbers, which further inflates the GMP — a classic self-reinforcing bubble.

On listing day, the manipulators sell their shares to the flood of retail buyers, pocket their profits, and the stock crashes within days or weeks. The retail investor who applied based on GMP is left holding a stock that’s 30-50% below the IPO price.

The rule: Never — and I mean NEVER — make an investment decision based on GMP alone. GMP tells you absolutely nothing about the long-term business quality of a company.

Red Flag #5: Suspicious Subscription Numbers

You see headlines screaming “SME IPO subscribed 300x!” and think it must be a great company. But dig deeper. Who is subscribing? In many cases, the overwhelming subscription comes from the NII (Non-Institutional Investor) category — which includes HNIs who apply with borrowed money (funded positions) purely for listing gains.

The real test of quality is the QIB (Qualified Institutional Buyer) category subscription. QIBs include mutual funds, insurance companies, and foreign institutional investors — sophisticated investors with research teams. If the QIB category is undersubscribed or barely subscribed while the retail and NII categories are oversubscribed 100x+, it tells you that professional investors don’t see value in the IPO, but retail money is chasing it blindly.

Smart approach: Always check the category-wise subscription data. Strong QIB subscription (3x or above) from reputable institutional names is a positive signal. Weak QIB participation despite high retail frenzy is a warning sign.

Red Flag #6: No Clear Competitive Moat or Market Position

Many SME IPO companies operate in highly competitive, commoditized businesses — trading, basic manufacturing, sub-contracting, or small-scale services. They have no pricing power, no brand recognition, no patents, no switching costs, and no scale advantage. Their entire “growth story” depends on the promoter’s optimistic projections in the prospectus.

Contrast this with a company like Titan Biotech, which has built a genuine competitive position in the biotechnology and life sciences space over decades. It supplies agar, peptones, and culture media to pharmaceutical companies, research institutions, and diagnostic labs — a specialized niche with real barriers to entry and consistent demand regardless of economic cycles.

The moat test: Before applying to any SME IPO, answer these three questions honestly:

1. Can a competitor with ₹5 crores easily replicate this business? If yes, there’s no moat.

2. Does the company have any pricing power, or is it a price-taker? Price-takers rarely create wealth.

3. Would the company survive if its largest customer left? If one customer accounts for 30%+ of revenue, that’s dangerous concentration risk.

Red Flag #7: Post-Listing Promoter Behavior

This is something most investors never check, but it’s incredibly revealing. After the mandatory lock-in period expires (usually 6-18 months for SME IPOs), watch what the promoter does. If they start selling shares aggressively, it tells you everything about their confidence in the company’s future.

Also watch for these post-listing red flags: sudden changes in auditors (a classic sign that the company doesn’t want thorough scrutiny), frequent board changes, delay in filing quarterly results, and disproportionate increase in “other income” (which often masks declining core business performance).

Due diligence tip: After an SME IPO lists, don’t just track the price. Track the promoter holding every quarter through BSE filings. Declining promoter holding without a valid reason (like fundraising or ESOP dilution) is a sell signal.

The Right Way to Invest: Quality Over Hype

The fundamental principle of value investing — buying high-quality businesses at reasonable prices — applies even more strongly to the SME space. Instead of gambling on untested SME IPOs, consider this approach:

Wait for a track record: Let the SME company prove itself for at least 4-6 quarters after listing. Watch if the revenue and profit growth continues post-IPO (when window dressing is no longer needed). If the company delivers consistent results, you can buy from the secondary market at potentially better prices than the IPO.

Focus on already-listed quality small-caps: The Indian market has hundreds of already-listed small and micro-cap companies with 5-10+ year track records, proven management, and real businesses. Titan Biotech is a perfect example — a company that has been listed for years, has demonstrated consistent performance, and has rewarded patient investors with extraordinary returns (from around ₹55 to approximately ₹369 today).

Demand real numbers: Before investing in any small company (IPO or listed), check these five non-negotiable criteria: positive operating cash flow for at least 3 consecutive years, Return on Equity above 15%, debt-to-equity ratio below 0.5 (preferably zero debt), consistent revenue growth of 15%+ annually, and promoter holding above 50%.

The SEBI Warning That Every Investor Must Heed

SEBI has been increasingly concerned about SME IPO quality. The regulator has tightened norms, including increasing the minimum application size, mandating more disclosures, and scrutinizing draft prospectuses more carefully. But regulations can only do so much — the primary responsibility of protecting your capital lies with YOU.

Remember SEBI’s landmark finding: 93% of F&O traders lose money. Don’t let the SME IPO frenzy become another avenue for wealth destruction. Approach every IPO with skepticism, do thorough due diligence, and remember that the best investments are boring — consistent, well-managed companies that compound wealth quietly over decades.

Your Action Plan: 5 Steps Before Applying to Any SME IPO

Step 1: Read the entire Draft Red Herring Prospectus (DRHP), not just the summary. Pay special attention to the Risk Factors section — that’s where the truth hides.

Step 2: Verify the financials independently. Cross-check the company’s claimed revenue with its GST filings (available on the MCA website), check the ROC filings, and verify the auditor’s reputation.

Step 3: Research the promoter’s background thoroughly. Have they run businesses before? Have any of their previous ventures failed or faced regulatory action? A quick search on SEBI’s enforcement database and MCA can reveal a lot.

Step 4: Compare the valuation with listed peers. If the IPO is priced at 60x P/E while comparable listed companies trade at 20-25x P/E, you’re being asked to pay a massive premium for an unproven company.

Step 5: Ask yourself the Warren Buffett question: “Would I be happy holding this stock if the market closed for 5 years?” If the answer is no, don’t apply.

Learn Value Investing — The Real Path to Wealth

Instead of chasing quick listing gains in SME IPOs, invest your time in learning value investing. Our comprehensive value investing course covers everything from fundamental analysis to identifying multibagger stocks the right way.

📚 Watch our free Value Investing Course: Complete Value Investing Course Playlist

Quality investing always wins in the long run. While F&O traders lost ₹1.8 lakh crores and SME IPO gamblers saw their capital erode, patient value investors who bought quality companies like Titan Biotech at reasonable valuations have seen their wealth multiply. The choice is yours.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. The author, Manish Goel, is an investor in Titan Biotech Ltd. Always conduct your own research and consult a SEBI-registered investment advisor before making any investment decisions. Stock market investments are subject to market risks — read all scheme-related documents carefully.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}