The Narrative Fallacy in Stock Analysis: Why Indian Investors Fall for Compelling Stories Instead of Hard Numbers — And How This Bias Destroys Wealth While You Think You’re Being Smart

The Biotech Gold Rush of 2026: How Biopharma SHAKTI and AI Are Creating a Once-in-a-Generation Investment Opportunity

March 28, 2026

Return on Assets (ROA): The Underrated Efficiency Metric That Reveals Whether Indian Companies Are Truly Creating Wealth — A Complete Guide for Smart Investors

March 29, 2026

March 29, 2026

(Sunday)

What Is the Narrative Fallacy — And Why Should Every Indian Investor Fear It?

Nobel laureate Daniel Kahneman, in his groundbreaking book Thinking, Fast and Slow, introduced a concept that has quietly destroyed more investor wealth than any stock market crash: the narrative fallacy.

The narrative fallacy is our brain’s irresistible urge to weave coherent, cause-and-effect stories from random, incomplete, or unrelated data points. Our minds are story-making machines — we cannot tolerate randomness. When we see a stock price going up, our brain demands a story to explain why. And once that story is in place, we become blind to contradictory evidence.

As Nassim Nicholas Taleb, who coined the term “narrative fallacy” in The Black Swan, explains: “We like stories, we like to summarize, and we like to simplify — i.e., to reduce the dimension of matters.” This is incredibly dangerous when your hard-earned money is at stake.

With the Sensex currently at 73,558 and Nifty around 23,058 (as of March 27, 2026), and with India VIX surging to 27.17 — its highest level since June 2024 — stories are flying everywhere. “India is finished,” “This is the start of a bear market,” “Buy the dip, India always recovers.” Each of these is a narrative. None of them are analysis.

How the Narrative Fallacy Works in the Indian Stock Market

Let me show you exactly how this bias operates with real Indian market examples:

Example 1: The “India Growth Story” Narrative (2021)

In 2021, when markets were booming post-COVID, the dominant narrative was: “India is the fastest-growing major economy, digital transformation is accelerating, and Indian stocks will only go up.” This narrative made investors pile into overvalued stocks at P/E ratios of 80-100x without checking basic fundamentals. Many of those stocks — particularly in the new-age tech space — have since fallen 60-80% from their highs.

The story was compelling. The numbers were not.

Example 2: The “Infrastructure Boom” Narrative

Every election cycle, the “India infrastructure boom” narrative returns. Investors rush to buy infrastructure stocks at any price because the story sounds amazing — highways, railways, smart cities. But seasoned value investors know that many infrastructure companies have terrible balance sheets, negative free cash flow, and a history of capital destruction. The story sells. The spreadsheet tells a different tale.

Example 3: The Right Way — Numbers First, Story Second

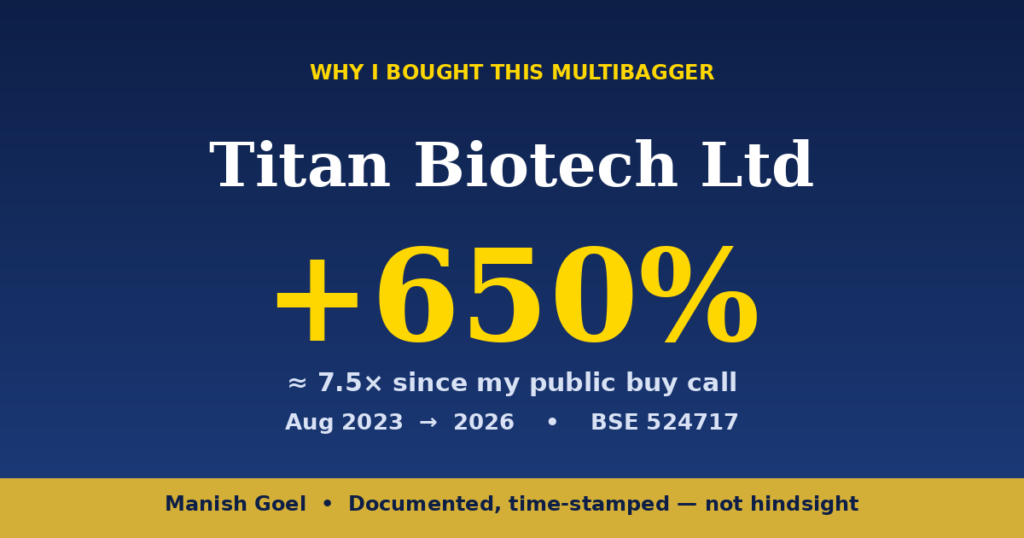

Consider Titan Biotech Ltd (BSE: 524717), currently trading around ₹368 with a market cap of approximately ₹305 crore. This stock wasn’t discovered through a compelling narrative — it was discovered through cold, hard numbers: consistent revenue growth, improving margins, debt-free balance sheet, high promoter holding, and strong return on equity. The narrative of India’s biotech boom came after the numbers confirmed the quality. That’s the correct order.

Titan Biotech’s net profit jumped 94.31% year-over-year in Q3 FY2025-26 to ₹8.53 crore. The stock has delivered over 326% returns in the past year. But the key insight is this: investors who bought based on numbers got in early. Investors who waited for a narrative bought much later, at much higher prices.

The Five Deadliest Forms of Narrative Fallacy in Stock Analysis

1. The “Visionary CEO” Story

A charismatic founder tells a beautiful story about disrupting an industry. Investors pour money in without checking whether the company has ever generated a single rupee of free cash flow. The story of the CEO becomes a substitute for financial analysis. Remember: a great story and ₹10 will buy you a cup of chai. Only great numbers will buy you wealth.

2. The “Sector Tailwind” Story

When a sector becomes hot — EV, AI, green energy, defence — every company in that sector gets a narrative boost. Investors buy the worst company in a hot sector rather than the best company in a boring sector. This is pure narrative fallacy. SEBI data shows that over 90% of F&O traders lose money, and a significant reason is that they chase sector narratives instead of analysing individual company fundamentals.

3. The “Past Performance Extrapolation” Story

A stock has gone up 500% in three years. The narrative becomes: “This company is a wealth-creating machine, it will keep compounding.” But was the 500% rise due to genuine earnings growth, or was it P/E expansion driven by narrative? If a stock went from a P/E of 10x to 50x, the “story” did most of the heavy lifting — and stories can reverse overnight.

4. The “Macro Doom” Story

Right now, with US-Iran tensions, Goldman Sachs downgrading India’s GDP growth to 5.9%, and FII outflows of ₹4,367 crore on March 27 alone, the doom narrative is powerful. “India is going to crash further,” “Recession is coming.” But the narrative ignores that DII inflows were ₹3,566 crore on the same day, that India’s structural growth story remains intact, and that the best time to buy quality stocks has historically been when narratives are most negative.

5. The “This Time It’s Different” Story

Perhaps the most dangerous narrative of all. Every bubble is accompanied by an explanation for why traditional valuation metrics don’t apply anymore. “This time, revenue growth matters more than profits.” “This time, the metaverse changes everything.” These four words — “this time it’s different” — have destroyed more wealth than any bear market in history.

Kahneman’s Framework: System 1 vs. System 2 in Stock Analysis

Kahneman’s research shows that our brains operate in two modes:

System 1 is fast, automatic, and story-driven. It’s the part of your brain that reads a headline like “AI company revenue doubles” and immediately wants to buy the stock. System 1 loves narratives. It creates them automatically and believes them instantly.

System 2 is slow, deliberate, and analytical. It’s the part that opens the annual report, checks the cash flow statement, calculates the return on equity, and asks “but what’s the debt level?” System 2 loves numbers. It’s skeptical of stories.

The problem? System 1 is always on. System 2 requires effort. Most investors — Kahneman estimates the vast majority — make investment decisions using System 1. They buy stocks because the story feels right, not because the numbers are right.

As Kahneman himself observed: “On average, people know very little about the stock market and yet feel they know a lot about it.” This overconfidence is fueled entirely by narrative.

The Anti-Narrative Checklist: A Practical Tool for Indian Investors

Before you invest a single rupee in any stock, run through this checklist to protect yourself from the narrative fallacy:

Step 1: Write Down the Story — What narrative is driving your interest in this stock? Be honest. Is it a tip from a friend? A YouTube video? A broker’s report? A news headline?

Step 2: Cover the Story, Read the Numbers — Open the company’s latest annual report. Ignore the Chairman’s message (that’s narrative). Go straight to the financial statements. Check revenue growth, profit margins, free cash flow, debt levels, return on equity, and promoter holding. Do the numbers independently support an investment?

Step 3: Perform a Pre-Mortem — This is Kahneman’s most powerful technique. Imagine it’s two years from now and your investment has lost 50% of its value. Write down the three most likely reasons this happened. If those reasons seem plausible, the narrative may be masking real risks.

Step 4: Find the Counter-Narrative — For every bullish story, there’s a bearish one. Actively seek out the bearish case. If you can’t find anyone who disagrees with your thesis, you’re probably in a narrative bubble.

Step 5: Check the Base Rate — What percentage of companies in this sector have actually delivered consistent returns over 10 years? Kahneman calls this the “outside view.” If 90% of companies in a sector have failed to generate returns, your narrative about why this company is different needs extraordinarily strong numerical support.

How Legendary Investors Defeat the Narrative Fallacy

Warren Buffett famously said: “You don’t need to be a rocket scientist. Investing is not a game where the guy with the 160 IQ beats the guy with the 130 IQ.” What beats IQ is temperament — the ability to resist compelling stories and stick to what the numbers say.

Charlie Munger developed his “mental models” framework specifically to combat narrative-driven thinking. By applying multiple analytical frameworks to every investment, you reduce the chance that any single narrative will dominate your decision-making.

Mohnish Pabrai, one of the most successful value investors in the world, uses a deceptively simple approach: he looks for situations where the downside is limited and the upside is significant — based entirely on numbers, not stories. His “Dhandho” framework is inherently anti-narrative.

The Indian Market Today: Separating Narrative from Reality

As we navigate March 2026 with the Sensex at 73,558, here’s the reality behind the current narratives:

Narrative: “India is crashing, get out of stocks.” Reality: India’s structural growth drivers — demographics, digitization, manufacturing shift from China — remain intact. Short-term FII selling driven by geopolitical events does not change the 10-year investment case.

Narrative: “Buy everything, this is a dip.” Reality: Not all stocks are equally attractive at current levels. Quality companies with strong cash flows and low debt (like Titan Biotech) represent genuine value. Overvalued growth stocks that were propped up by narrative alone may have further to fall.

The right approach? Let numbers be your guide, not narratives. Open the balance sheet before you open Twitter. Calculate the intrinsic value before you listen to the “expert” on TV. Check the free cash flow before you check the stock price chart.

Why F&O Trading Is the Ultimate Narrative Trap

Futures and Options trading is essentially betting on short-term narratives. “Nifty will bounce from support.” “Bank Nifty will break out.” These are stories, not analysis. SEBI’s landmark study revealed that over 90% of individual F&O traders lose money, with average losses of ₹50,000 per person. The reason? F&O traders are the ultimate victims of narrative fallacy — they construct stories about where the market will go next, and they bet real money on these stories.

Quality investing in fundamentally strong companies — buying businesses with real earnings, real cash flows, and real competitive advantages — is the only proven path to long-term wealth creation. Don’t gamble your future on stories. Build it on numbers.

Your Action Plan: Becoming a Numbers-First Investor

Starting today, make this commitment: every time you feel the urge to buy a stock, ask yourself one question — “Am I buying this because of a story, or because of the numbers?”

If the answer is “story,” stop. Open the annual report. Run the numbers. Apply the anti-narrative checklist. Only if the numbers independently confirm value should you proceed.

This single discipline — putting numbers before narratives — is what separates the investors who build generational wealth from those who donate their savings to the stock market.

As Daniel Kahneman taught us: the world makes a lot less sense than you think. The coherence of the story is not a guarantee of its truth. In investing, the most dangerous stories are the ones that feel the most true.

Disclaimer: This blog post is for educational purposes only and does not constitute financial advice. The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). All investments carry risk. Please consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Read all related documents carefully. Past performance is not indicative of future results.

📺 Want to learn value investing from scratch? Watch our complete FREE course: Value Investing Course Playlist

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}