Anchoring Bias: The Invisible Mental Trap That Makes Indian Investors Buy Too High and Sell Too Low — How to Recognize and Defeat the #1 Pricing Illusion in Stock Markets

Sum-of-the-Parts (SOTP) Valuation: The Advanced Method to Uncover Hidden Value in Diversified Indian Conglomerates — Why the Whole Can Be Worth LESS Than the Sum of Its Parts and How Smart Investors Profit from the Gap

April 1, 2026

Confirmation Bias: The Silent Portfolio Killer That Makes Indian Investors See Only What They Want to See — And How to Break Free Before It Destroys Your Wealth

April 1, 2026

April 01, 2026

(Tuesday)

Why Your Brain Is Your Worst Enemy When Pricing Stocks

Today, on April 1, 2026, the Indian stock market delivered a powerful rally — the Sensex surged to 73,134 (up 1.65%) and the Nifty 50 climbed to 22,679 (up 1.56%), fueled by easing geopolitical tensions and falling crude oil prices. Amid this euphoria, thousands of Indian investors are making a critical mistake without even realizing it.

They are anchoring.

Right now, as you read this, your brain is silently referencing an irrelevant number — a past stock price, a 52-week high, a friend’s purchase price, an analyst’s old target — and letting that number dictate whether you think a stock is “cheap” or “expensive.” This is called anchoring bias, and it is arguably the most dangerous behavioral trap in investing.

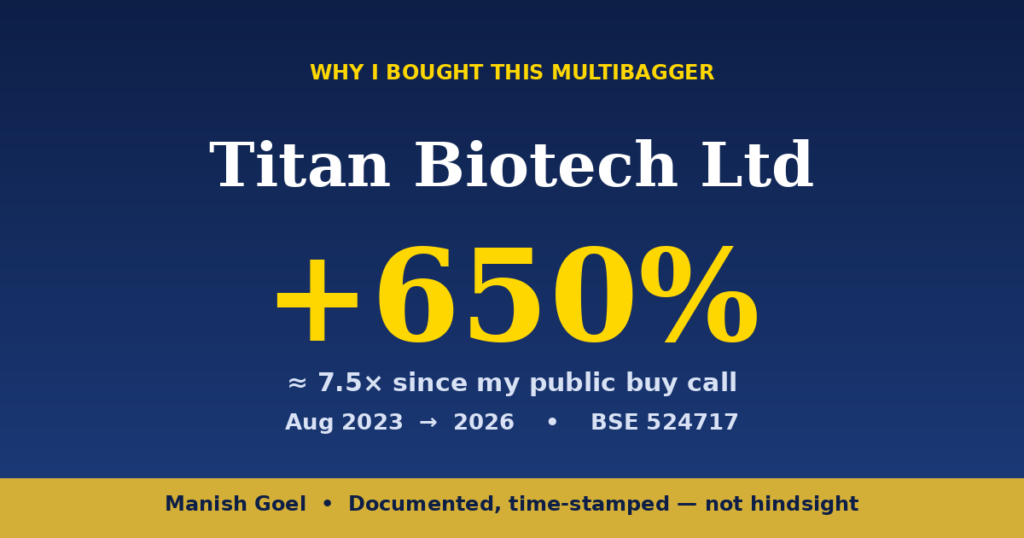

In this comprehensive guide, we will dissect exactly how anchoring bias works, why it’s especially destructive in the Indian stock market, and how you can train your mind to defeat it. Along the way, we’ll examine real examples — including the remarkable journey of Titan Biotech (BSE: 524717), currently trading at ₹480.00 (up 4.87% today) with a market cap of ₹396.67 Crore — to illustrate why anchoring to past prices is the fastest way to miss future multibaggers.

What Exactly Is Anchoring Bias?

Anchoring bias is a cognitive phenomenon where people rely too heavily on the first piece of information they encounter (the “anchor”) when making subsequent decisions. Nobel laureates Daniel Kahneman and Amos Tversky first documented this effect in their groundbreaking 1974 paper, and it has since become one of the most replicated findings in behavioral science.

In investing, anchoring manifests in several dangerous ways:

Price Anchoring: “I won’t buy Stock X because it was ₹200 last year and now it’s ₹400 — it’s too expensive.” The investor is anchoring to the old price instead of evaluating the current fundamentals. What if the company’s earnings doubled? What if a transformational event — like Titan Biotech’s entry into semaglutide APIs — fundamentally changed the business’s trajectory? The ₹200 price is irrelevant to today’s intrinsic value.

52-Week High/Low Anchoring: Many investors refuse to buy a stock near its 52-week high, believing it “must” come down. Consider Titan Biotech: its 52-week high is ₹480.55 and its 52-week low is ₹74.73. An investor anchoring to the low of ₹74.73 might think ₹480 is absurdly expensive. But the company’s ROCE stands at 16.72%, ROE at 12.74%, promoter holding is a healthy 55.78%, and the business fundamentals have transformed dramatically. The ₹74.73 price reflects a completely different reality.

Purchase Price Anchoring: This is perhaps the most common form. Once you buy a stock at a certain price, that price becomes your “anchor.” If the stock falls to ₹150, you think it’s a disaster. If it rises to ₹500, you think it’s time to sell. Neither reaction is based on what the stock is actually worth today — both are anchored to your entry price.

Analyst Target Anchoring: When a broker gives a target price of ₹600, that number sticks in your mind. Even if the company’s fundamentals deteriorate, you hold on waiting for ₹600. Conversely, if fundamentals improve dramatically and the fair value is now ₹1,000, you sell at ₹600 because you’ve anchored to the old target.

The Science Behind Why Anchoring Is So Powerful

Anchoring works because of how our brains process information. When faced with uncertainty (and stock prices are inherently uncertain), the brain takes a mental shortcut: it starts with an available reference point and adjusts from there. The problem is that the adjustment is almost always insufficient.

In a famous experiment, Kahneman and Tversky spun a wheel that randomly landed on either 10 or 65. They then asked participants to estimate the percentage of African countries in the United Nations. People who saw “10” on the wheel guessed around 25%. People who saw “65” guessed around 45%. A completely random number influenced their estimate of a factual question!

Now imagine how powerfully a real number — like a stock’s previous price — influences your perception of its value. The effect is enormous, and even professional fund managers fall prey to it.

How Anchoring Bias Destroys Wealth in Indian Markets

The Indian stock market is particularly susceptible to anchoring bias for several reasons:

1. The “It Was Cheaper Before” Syndrome: India has produced some of the greatest wealth-creating stocks in history — companies like Asian Paints, Bajaj Finance, and HDFC Bank. Yet at every stage of their journey, anchoring bias caused investors to sell too early. “Asian Paints was ₹50 when I first looked at it. Now it’s ₹300 — too expensive!” That investor missed a 100x return because they anchored to an irrelevant past price.

2. IPO Price Anchoring: Indian investors are notorious for anchoring to IPO prices. If an IPO was listed at ₹100 and the stock is now at ₹80, they think it’s “cheap” and a good buy. But the IPO price was set by investment bankers to maximize the company’s fundraise — it has zero relationship to intrinsic value. Many SME IPOs in India were priced at absurd valuations, and anchoring to those prices has destroyed enormous retail wealth.

3. Round Number Anchoring: Notice how Indian investors obsess over Sensex at 75,000 or Nifty at 25,000? These round numbers become powerful psychological anchors. When Sensex approaches a round number, media frenzy creates buying pressure. When it falls below one, panic selling follows. Today, with Sensex at 73,134 after the recent correction from higher levels, many investors are anchoring to those previous highs instead of evaluating whether current valuations offer good value.

4. SEBI’s Sobering Warning: According to SEBI’s own study, 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses. Many of these losses are amplified by anchoring — F&O traders anchor to their entry price and refuse to cut losses, watching small mistakes compound into devastating ones. This is why we always emphasize: F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

The Titan Biotech Lesson: Why Anchoring to Old Prices Means Missing Multibaggers

Let’s examine how anchoring bias has played out with Titan Biotech (BSE: 524717) — a company we’ve studied extensively on this platform.

Titan Biotech, currently trading at ₹480.00 with a market cap of ₹396.67 Crore, has delivered extraordinary returns. The stock’s 52-week low is just ₹74.73, meaning an investor who bought at the low would have earned over 540% returns in less than a year.

But here’s where anchoring bias strikes: an investor who first noticed Titan Biotech at ₹100 (post-split) and didn’t buy, now anchors to that ₹100 price. When the stock hits ₹200, they think “it’s doubled, too expensive.” At ₹300, they feel vindicated in not buying. At ₹480, they’re convinced it’s going to crash.

Meanwhile, the fundamentals tell a completely different story. The company’s ROCE of 16.72% and ROE of 12.74% demonstrate genuine business quality. Promoter holding at 55.78% shows skin-in-the-game confidence. The company operates in the high-growth biopharma ingredients space — a sector benefiting from India’s Biopharma SHAKTI initiative and the global shift in API manufacturing to India.

The lesson is clear: price is what you pay, value is what you get. Anchoring to past prices instead of evaluating current and future value is how investors miss the greatest wealth-creating opportunities.

Five Practical Strategies to Defeat Anchoring Bias

Now that you understand the danger, here are five battle-tested strategies to protect yourself:

Strategy 1: Always Start with Intrinsic Value, Never with Price. Before looking at any stock’s current price or price history, first estimate its intrinsic value based on fundamentals — earnings, cash flows, growth rates, and competitive position. Only after you have an independent estimate should you check the market price. This way, your valuation is anchored to fundamentals, not to an arbitrary market price.

Strategy 2: Use Multiple Valuation Methods. Don’t rely on a single valuation approach. Use DCF analysis, relative valuation (P/E, EV/EBITDA compared to peers), and asset-based approaches. If all three methods give you a similar range, you can be more confident your estimate isn’t distorted by anchoring to any single metric.

Strategy 3: Practice “Consider the Opposite.” Whenever you catch yourself thinking “this stock is too expensive because it was cheaper before,” force yourself to ask: “What if the old price was too cheap? What if the market was undervaluing the company then, and is only now recognizing its true worth?” This simple mental exercise breaks the anchor’s hold.

Strategy 4: Write Down Your Thesis Before Buying. Document exactly why you’re buying a stock, what fundamentals support your decision, and what specific events or metrics would cause you to sell. This written record gives you a fundamental anchor to replace the price anchor. When the stock moves, you can check your thesis instead of checking the price chart.

Strategy 5: Review Your Portfolio by Fundamentals, Not by P&L. Instead of checking whether your stocks are up or down (which anchors you to your purchase price), review each position by asking: “Would I buy this stock today at this price?” If the answer is yes, hold. If no, sell. This removes your purchase price from the equation entirely.

How the Best Investors in History Have Conquered Anchoring

Warren Buffett has famously said: “Price is what you pay, value is what you get.” This deceptively simple statement is actually a powerful anti-anchoring philosophy. Buffett doesn’t care what a stock traded at yesterday, last month, or last year. He cares what the underlying business is worth based on its future cash flows.

When Buffett bought Coca-Cola shares in 1988, the stock had already risen significantly from its lows. Many investors would have been anchored to the lower prices and refused to buy. But Buffett analyzed the business value and concluded it was still undervalued. He went on to earn billions from that investment.

Similarly, in Indian markets, the late Rakesh Jhunjhunwala was known for buying stocks at what others considered “high” prices — because he was anchored to business value, not market price. His famous investment in Titan Company was made when many thought the stock was already expensive. The rest is history.

The Market Context: Why Understanding Anchoring Matters MORE Today

Today’s market rally — with the Sensex surging to 73,134 and the Nifty climbing to 22,679 — comes after a period of significant volatility driven by geopolitical tensions. Many investors are now anchoring to the recent lows and thinking the rally is “overdone.” Others are anchoring to previous all-time highs and thinking we have more room to run.

Both camps are making the same mistake: they’re letting irrelevant past prices determine their investment decisions instead of evaluating individual companies on their merits.

The disciplined value investor ignores the noise and asks: “Is this specific company — with these specific fundamentals, this management quality, this competitive position — worth more or less than its current market price?” That’s the only question that matters.

Your Action Plan: Breaking Free from the Anchor

Starting today, commit to these three habits:

First, never say a stock is “cheap” or “expensive” based on where it used to trade. A stock is only cheap or expensive relative to its intrinsic value — not relative to its historical price.

Second, build your value investing knowledge systematically. If you’re serious about learning to evaluate stocks on fundamentals rather than falling for behavioral traps, explore our comprehensive Value Investing Course on YouTube — it’s completely free and designed specifically for Indian investors.

Third, always remember SEBI’s sobering statistic: 9 out of 10 F&O traders lose money. Much of this is due to behavioral biases like anchoring. The path to wealth creation in Indian markets isn’t through speculation — it’s through disciplined, fundamental-driven value investing in quality companies.

The market doesn’t care what price you paid. It doesn’t care what price the stock used to be. It only cares about the future cash flows of the business. Once you internalize this truth, you’ve taken the first step toward breaking free from the invisible chains of anchoring bias.

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}