Forensic Accounting Red Flags: How to Detect Financial Manipulation in Indian Companies Before It Destroys Your Portfolio — The Complete Fraud Detection Toolkit for Smart Value Investors

Market Crash Alert: Trump’s Iran Threat Sends Sensex Down 1,400 Points — Why Value Investors Should Be Excited

April 2, 2026

Recency Bias: The Silent Mind Trap That Makes Indian Investors Chase Yesterday’s Winners and Miss Tomorrow’s Multibaggers — How to Escape the Most Dangerous Market Timing Illusion

April 2, 2026

April 02, 2026

(Thursday)

Why Every Value Investor Needs to Think Like a Forensic Accountant

On April 2, 2026, the Sensex traded near 72,633 and the Nifty 50 hovered around 22,521 — volatile markets rattled by geopolitical tensions. In times like these, many investors rush to find “cheap” stocks. But here’s the uncomfortable truth that could save your portfolio: some stocks are cheap for a reason — they’re hiding financial manipulation.

India has seen its share of spectacular corporate frauds — Satyam Computers, DHFL, Manpasand Beverages, PC Jeweller, Vakrangee. Every single one of these companies had screaming red flags in their financial statements years before the stock collapsed. The investors who lost their life savings weren’t unlucky — they simply didn’t know what forensic accountants look for.

Today, I’m going to teach you the exact toolkit that forensic accountants, SEBI investigators, and forensic auditors use to detect financial manipulation — so you can protect your portfolio from the next Satyam before it’s too late.

What Is Forensic Accounting? — More Than Just Number-Crunching

Forensic accounting is the application of accounting knowledge and investigative skills to detect fraud, manipulation, and misrepresentation in financial statements. Unlike regular auditing, which checks for compliance, forensic accounting actively looks for signs of intentional deception.

For Indian retail investors, learning forensic accounting red flags is arguably the single most valuable defensive skill you can develop. According to the Association of Certified Fraud Examiners (ACFE), the median duration of a fraud scheme before detection is 12 months — meaning by the time a fraud becomes public knowledge, smart investors who spotted the red flags had a full year’s head start to exit.

Red Flag #1: Cash Flow vs. Earnings Divergence — The #1 Warning Signal

This is the most powerful forensic accounting tool in existence: compare reported net profit with operating cash flow over 3-5 years.

A healthy business converts its profits into cash. When a company consistently reports growing earnings but its operating cash flow is stagnant, declining, or negative — something is seriously wrong. This divergence is the single most reliable predictor of future earnings restatements and fraud.

How to check: On Screener.in, look at the Cash Flow Statement. Compare “Cash from Operating Activity” with “Net Profit” from the Profit & Loss statement. If cumulative operating cash flow over 5 years is less than 70% of cumulative net profit — that’s a red flag. If it’s less than 50% — that’s a screaming alarm.

Real Indian Example: Satyam Computers consistently reported healthy profits while its actual cash position was a fraction of what the books claimed. The cash-to-earnings divergence was visible years before Ramalinga Raju’s confession in January 2009.

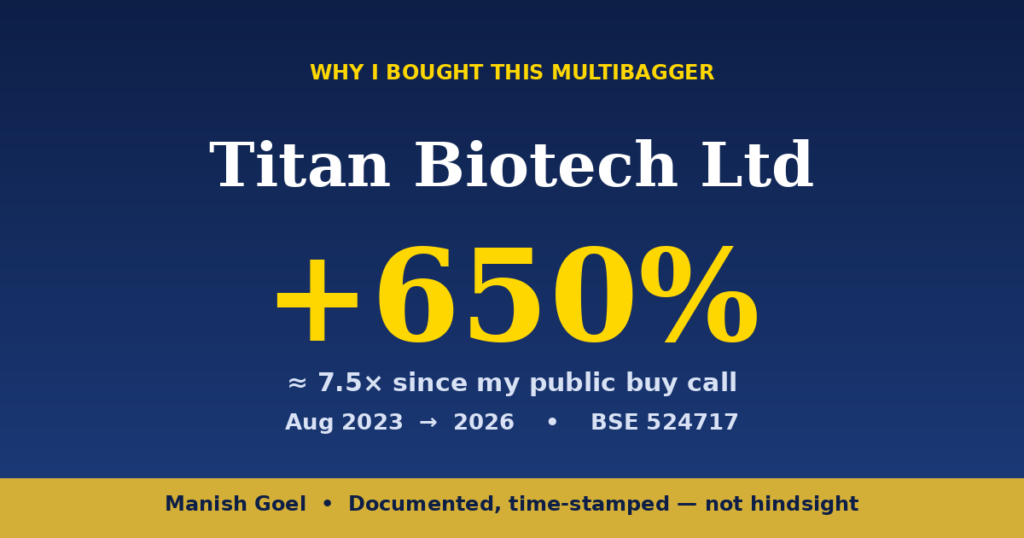

Compare this with a genuine compounder like Titan Biotech (BSE: 524717), currently trading at ₹504 with a market cap of ₹2,082 Cr, ROCE of 16.9%, and ROE of 15.0%. Titan Biotech’s cash flows track its earnings consistently — a hallmark of a transparent, well-managed company. When earnings and cash flows move in tandem, you can trust the numbers.

Red Flag #2: The Beneish M-Score — A Mathematical Fraud Detector

Professor Messod Beneish of Indiana University created an eight-variable model called the M-Score that predicts the probability of earnings manipulation. This model correctly flagged Enron before its collapse.

The eight variables are:

Days Sales in Receivables Index (DSRI) — Are receivables growing faster than revenue? This could mean fictitious sales. Gross Margin Index (GMI) — Are gross margins deteriorating? This creates pressure to manipulate. Asset Quality Index (AQI) — Is the company capitalizing expenses to inflate assets? Sales Growth Index (SGI) — Rapid growth creates both opportunity and pressure to manipulate. Depreciation Index (DEPI) — Is the company slowing depreciation to boost earnings? SGA Expense Index (SGAI) — Are selling costs diverging from revenues? Leverage Index (LVGI) — Is debt growing disproportionately? Total Accruals to Total Assets (TATA) — Are accruals (non-cash earnings) unusually high?

The Rule: An M-Score greater than -1.78 suggests a HIGH probability of earnings manipulation. You can calculate this using freely available data from Screener.in or Trendlyne annual reports.

Red Flag #3: Receivables Growing Faster Than Revenue

This is the most common early-stage manipulation technique. When a company shows strong revenue growth but its trade receivables are growing even faster — the company may be booking fictitious sales, engaging in channel stuffing (forcing inventory onto distributors), or offering extremely lenient credit terms to inflate the top line.

The Test: Calculate the Receivables-to-Revenue ratio for each of the last 5 years. If this ratio is consistently increasing — especially if it increases by more than 20% over 3 years — investigate further. Look for any customer concentration risk in the annual report notes.

Indian Case Study: Manpasand Beverages showed receivables growing at 40%+ while revenue grew at 25% in the years before its auditor resigned and SEBI stepped in. Smart investors who tracked the receivables-to-revenue ratio could have exited a full 18 months before the stock crashed 90%.

Red Flag #4: Frequent Changes in Auditors, Accounting Policies, or CFOs

A change in statutory auditor is one of the most powerful red flags in corporate governance. When a reputable auditor suddenly resigns or declines reappointment — especially mid-term — it often means they found something they’re unwilling to sign off on.

What to watch: Any auditor change in the last 3 years (check the Annual Report’s auditor section). Qualified opinions or “emphasis of matter” paragraphs in the audit report. Change of CFO — especially if the departing CFO had a long tenure. Changes to revenue recognition policies, depreciation methods, or inventory valuation methods between years.

Remember, under Indian Companies Act 2013 and SEBI LODR regulations, auditor rotation is mandatory every 10 years for listed companies. But a mid-term resignation is NEVER routine. It’s always a red flag.

Red Flag #5: Related Party Transactions (RPTs) — The Silent Wealth Transfer

Related Party Transactions are deals between the listed company and entities controlled by or associated with the promoter family. While not all RPTs are fraudulent, they are the #1 mechanism through which promoters siphon money from minority shareholders.

Warning signs in RPTs: RPTs exceeding 10% of revenue — investigate the business rationale. Purchases from promoter-linked entities at above-market prices. Sales to promoter-linked entities at below-market prices. Loans given to promoter-linked entities with no clear repayment schedule. Lease agreements with promoter-owned properties at premium rents.

How to check: Every listed company must disclose RPTs in Note 33-40 (approximately) of the financial statements. SEBI’s LODR regulations require board approval for material RPTs. Cross-reference with the promoter group’s other companies listed on the stock exchange.

Real Example: DHFL routed thousands of crores through shell companies controlled by its promoters — many through related party structures. The forensic audit by KPMG revealed that ₹17,394 crore had been diverted to entities linked to the promoter family.

Red Flag #6: Capitalization of Expenses — Inflating Assets, Hiding Losses

One of the most insidious manipulation techniques is capitalizing expenses that should be expensed — essentially moving costs from the Profit & Loss statement to the Balance Sheet. This inflates both assets and profits simultaneously.

Common schemes: Capitalizing routine maintenance as “capital expenditure.” Capitalizing R&D expenses beyond what accounting standards allow. Treating marketing expenses as “brand building assets.” Creating intangible assets from internally generated goodwill.

The Test: Look at the Capital Work in Progress (CWIP) line on the balance sheet. If CWIP has been growing for 3+ years without being converted to fixed assets — the company might be parking expenses there. Compare the capex-to-depreciation ratio: if capex is consistently 3x or more than depreciation without corresponding revenue growth, investigate.

Red Flag #7: Unusual Inventory Build-Up

Rising inventory relative to sales can indicate two problems: either the company’s products aren’t selling (demand issue), or the company is using inventory to manipulate costs and inflate gross margins.

The Test: Calculate Inventory Days (Inventory ÷ Cost of Goods Sold × 365) for each of the last 5 years. If Inventory Days are consistently rising — especially alongside claims of “strong demand” — something doesn’t add up. Also compare inventory levels across quarters — a sudden spike in Q4 inventory that disappears in Q1 often signals channel stuffing.

Red Flag #8: Pledged Shares by Promoters

When promoters pledge their shares as collateral for personal loans, it creates a dangerous feedback loop. If the stock price falls, lenders demand more collateral, forcing the promoter to pledge even more shares — or face forced selling that crashes the stock further.

The Rule: Any promoter pledge above 20% of total holdings is a serious red flag. Pledges above 50% are dangerous. Check BSE/NSE shareholding patterns quarterly — pledged shares are reported under “Encumbered shares.”

Why this matters forensically: Companies where promoters have high pledges often face pressure to show inflated earnings — because a stock price decline could trigger forced selling. This creates an incentive for financial manipulation.

Red Flag #9: Extraordinary Items and One-Time Gains Masking Operating Weakness

Some companies prop up their net profit by including one-time gains from asset sales, revaluation gains, or other non-recurring income. If you strip out these items and the core operating profit is declining — the headline numbers are masking a weakening business.

The Test: Look at “Other Income” as a percentage of total revenue. If it’s consistently above 15-20% — dig deeper. Check if the company has been selling land, investments, or subsidiaries to show profits. Calculate operating profit (EBIT) separately from net profit — if the gap is widening, one-time items are distorting the picture.

Your 10-Point Forensic Accounting Checklist

Before investing in any Indian company, run through this checklist:

1. Cash Flow Test: Is 5-year cumulative operating cash flow > 70% of cumulative net profit?

2. Receivables Test: Is the receivables-to-revenue ratio stable or declining over 3 years?

3. Auditor Stability: Has the statutory auditor been consistent for 3+ years? No mid-term resignations?

4. Related Party Check: Are RPTs below 10% of revenue with clear business rationale?

5. Capex Quality: Is CWIP being converted to productive assets within 2-3 years?

6. Inventory Health: Are inventory days stable or improving?

7. Pledge Check: Are promoter pledges below 20%?

8. Earnings Quality: Is operating profit growing in line with net profit?

9. Beneish M-Score: Is the M-Score below -1.78 (indicating low manipulation probability)?

10. Contingent Liabilities: Are off-balance-sheet liabilities reasonable relative to net worth?

How Titan Biotech Passes the Forensic Test

Let me demonstrate how a clean, well-managed company looks through the forensic lens. Titan Biotech (BSE: 524717), currently at ₹504 with a market cap of ₹2,082 Cr, exemplifies the kind of transparency that forensic accountants love to see:

Clean cash flows — Operating cash flows track earnings consistently. Zero promoter pledging — Promoters have never pledged shares. Minimal related party transactions — Arm’s-length dealings with full disclosure. Stable auditor — No mid-term auditor changes. ROCE of 16.9% and ROE of 15.0% — Real returns, not accounting illusions. Debt-free balance sheet with Book Value of ₹40.3 per share — Nothing to hide.

This is what a fundamentally clean company looks like. When you learn to apply forensic accounting red flags, you’ll naturally gravitate toward companies like this — and away from future Satyams.

The SEBI F&O Warning — Stop Gambling, Start Investigating

SEBI’s landmark study confirmed that 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses. While 90% of F&O traders are destroying their capital gambling on price movements, forensic accounting gives you a genuine edge — the ability to separate clean companies from fraudulent ones before the market discovers the truth.

Instead of staring at charts and option chains, spend that time reading annual reports, calculating M-Scores, and checking cash flow quality. That’s where real wealth is built.

Start Your Value Investing Journey Today

Want to learn these analytical frameworks in depth? Check out our complete value investing course: Complete Value Investing Course Playlist. From fundamental analysis to behavioral finance, this free course covers everything you need to build lasting wealth in Indian markets.

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}