Discounted Cash Flow (DCF) for Beginners: The Gold Standard Valuation Method That Tells You What Any Stock Is TRULY Worth — A Complete Step-by-Step Guide for Indian Investors

Price-to-Book (P/B) Ratio: The Fundamental Valuation Metric That Reveals Whether You’re Buying Indian Stocks at a Discount or Paying a Premium — A Complete Guide for Smart Value Investors

April 3, 2026

The Sunk Cost Fallacy: Why Indian Investors Keep Averaging Down on Failing Stocks — The Behavioral Trap That Costs Retail Investors Billions and How to Break Free

April 3, 2026

April 02, 2026

(Wednesday)

Why Every Indian Investor Needs to Understand DCF — The Only Valuation Method That Answers “What Is This Stock Really Worth?”

With the Sensex at approximately 72,633 and Nifty 50 around 22,521 today (April 2, 2026), markets remain volatile amid geopolitical tensions. In times like these, when prices swing wildly on headlines about Iran, tariffs, or FII outflows, one question separates the amateurs from the professionals: “What is this business actually worth?”

Most retail investors in India rely on shortcuts — they look at the P/E ratio, compare it with peers, and call it “valuation.” But P/E ratios are backward-looking. They tell you what the market paid yesterday, not what the business is worth tomorrow. The Discounted Cash Flow (DCF) model is fundamentally different. It is the only valuation method that values a business based on what it will generate for you in the future — and then converts those future cash flows into today’s rupees.

Warren Buffett himself has said: “Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.” This single sentence captures the entire philosophy behind DCF. Today, we will break it down from scratch — no MBA required.

What Is Discounted Cash Flow (DCF)?

At its core, DCF answers a deceptively simple question: If I could own this entire business and collect every rupee of free cash it generates for the next 10–15 years, how much would I pay for that stream of cash today?

The word “discounted” is the key. A rupee received 10 years from now is worth less than a rupee in your hand today — because of inflation, opportunity cost, and risk. DCF accounts for all three by applying a “discount rate” that shrinks future cash flows back to their present value.

The formula in its simplest form is:

Intrinsic Value = Σ [FCF₁/(1+r)¹ + FCF₂/(1+r)² + … + FCFₙ/(1+r)ⁿ] + Terminal Value/(1+r)ⁿ

Where FCF = Free Cash Flow in each year, r = discount rate (your required rate of return), and n = the number of years you’re projecting.

The Five Building Blocks of a DCF Model

Building Block 1: Free Cash Flow (FCF)

Free Cash Flow is the actual cash a business generates after paying for everything it needs to keep running and growing. The formula is:

FCF = Operating Cash Flow − Capital Expenditures (Capex)

Why FCF and not net profit? Because profits can be manipulated through accounting — depreciation policies, revenue recognition timing, one-time gains. Cash flow is much harder to fake. When Satyam Computer’s profits looked healthy, its cash flows told a completely different story. Indian investors who relied on reported earnings lost everything; those who checked cash flows saw red flags years earlier.

Building Block 2: Growth Rate Projection

You need to estimate how fast FCF will grow over the next 10 years. This is where your fundamental analysis skills matter. Look at historical revenue growth (5-year and 10-year CAGR), the industry’s structural growth runway, the company’s competitive advantages (pricing power, distribution network, brand), and management’s capital allocation track record.

For a high-quality Indian company, you might project 15–20% growth for the first 5 years and 10–12% for years 6–10. For a mature company, perhaps 8–12% throughout. The key rule: be conservative. It is far better to underestimate growth and find a bargain than to overestimate and overpay.

Building Block 3: The Discount Rate

The discount rate represents your minimum acceptable return — the rate at which you discount future cash flows back to the present. In academic finance, this is the Weighted Average Cost of Capital (WACC). For practical value investing in India, many investors use 12–15% as their discount rate because that represents a reasonable required return above the risk-free rate (currently ~7% on 10-year government bonds) plus an equity risk premium.

A higher discount rate makes the intrinsic value lower (you’re demanding a higher return, so you’ll pay less). A lower discount rate makes intrinsic value higher. This is why interest rate changes affect stock prices — when rates rise, discount rates rise, and intrinsic values fall.

Building Block 4: Terminal Value

You cannot project cash flows forever. After your explicit projection period (typically 10 years), you assume the company continues to grow at a steady, modest rate — usually 4–6% for an Indian company (roughly nominal GDP growth). This “perpetuity growth” phase gives you the Terminal Value:

Terminal Value = FCF in final year × (1 + perpetuity growth rate) / (discount rate − perpetuity growth rate)

WARNING: Terminal Value often accounts for 60–70% of a DCF’s total value. This means your perpetuity growth assumption has enormous impact. This is exactly why you should be conservative here — overestimating perpetuity growth by even 1% can inflate your valuation by 20–30%.

Building Block 5: Per-Share Intrinsic Value

Sum up all the discounted FCFs plus the discounted Terminal Value. This gives you the intrinsic value of the entire business. Divide by total shares outstanding to get the per-share intrinsic value. Then compare this number with the current market price — if the market price is significantly below your intrinsic value, you may have found a bargain.

A Simplified DCF Example — An Indian FMCG Company

Let us walk through a hypothetical example. Suppose “ABC Consumer Ltd” generates FCF of ₹500 crore this year. You estimate:

- FCF growth: 15% per year for the next 10 years

- Discount rate: 13%

- Perpetuity growth: 5%

- Shares outstanding: 50 crore

Year 1 FCF: ₹575 Cr → Discounted: ₹509 Cr. Year 2: ₹661 Cr → Discounted: ₹518 Cr. And so on for 10 years. The sum of all 10 years of discounted FCF might come to approximately ₹5,800 Cr. The Terminal Value (calculated using Year 10 FCF of ₹2,023 Cr, growing at 5%, discounted at 13%) would be approximately ₹7,900 Cr in present value terms. Total intrinsic value: ₹13,700 Cr. Per share: ₹274.

If ABC Consumer trades at ₹200, you have a significant margin of safety. If it trades at ₹350, it is overvalued by your estimates. This is the power of DCF — it gives you a specific number to anchor your buy/sell decisions instead of relying on market sentiment.

The Seven Deadly Mistakes Indian Investors Make with DCF

Mistake 1: Using Overly Optimistic Growth Rates. Just because a company grew at 25% for the last 3 years does not mean it will sustain that for a decade. Mean reversion is real. Always use conservative estimates and check what happens if growth is 5% lower than your base case.

Mistake 2: Ignoring Capex Cycles. Some industries (telecom, steel, cement) go through massive capex cycles. If you only use a “good year” FCF as your base, you will overestimate terribly. Use normalized or average FCF over a full business cycle.

Mistake 3: Using Too Low a Discount Rate. In India, with inflation running at 4–6% and equity risk premiums higher than developed markets, a discount rate below 12% is almost certainly too low. Using 8–9% (common in US-focused models) will make everything look cheap.

Mistake 4: Neglecting Working Capital Changes. A company might show growing profits but consume cash through increasing receivables or inventory. Always check that operating cash flow closely tracks operating profit. Companies where cash flow consistently lags profit are potential red flags.

Mistake 5: Terminal Value Dominance. If terminal value is more than 75% of your total DCF value, your model is essentially a bet on what happens after your projection period — which means you’re not really analyzing the business, you’re guessing about the distant future. Try to use companies where near-term cash flows contribute at least 30–40% of value.

Mistake 6: Not Running Sensitivity Analysis. A single DCF number is meaningless without knowing how sensitive it is to your assumptions. Always create a table: what is intrinsic value if growth is 10% vs 15% vs 20%? What if the discount rate is 12% vs 14% vs 16%? This range gives you intellectual honesty.

Mistake 7: Anchoring to DCF Results. Ironically, the biggest DCF mistake is treating your output as gospel. DCF is a thinking tool, not an oracle. It forces you to make explicit assumptions about the future — and that process of thinking is often more valuable than the final number.

When DCF Works Best — And When It Doesn’t

DCF works beautifully for: Stable, cash-generating businesses with predictable revenues — consumer staples, IT services, established pharma companies, well-run banks with consistent NIMs. These businesses have the kind of cash flow predictability that makes projections meaningful.

DCF struggles with: Early-stage companies with no positive cash flow, highly cyclical businesses (commodity producers, real estate developers), turnaround stories where the future bears no resemblance to the past, and financial companies where “cash flow” has different meanings.

For cyclical companies, use normalized earnings across a full cycle. For banks and NBFCs, use a Residual Income or Dividend Discount Model instead. For early-stage companies, consider revenue multiples or probability-weighted scenario analysis.

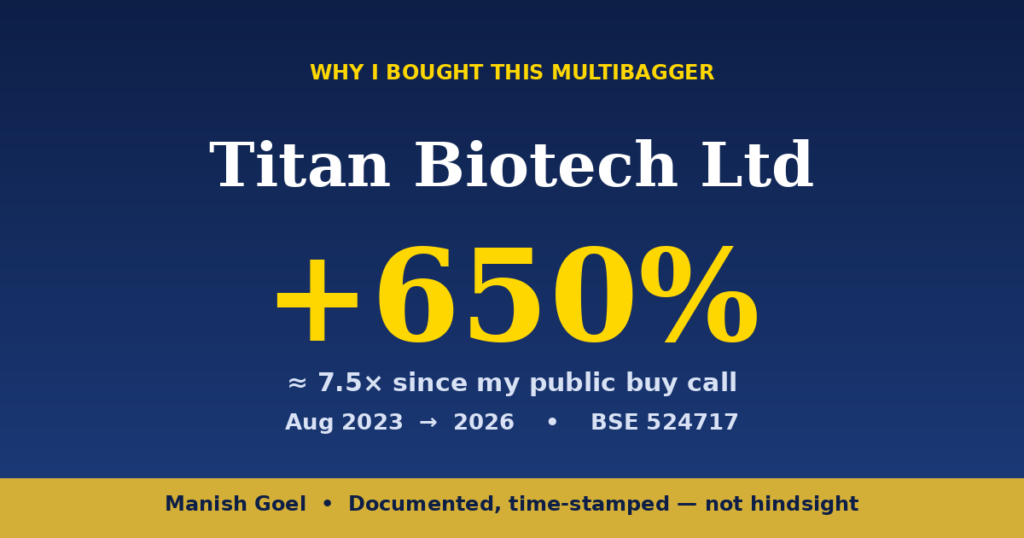

The Titan Biotech Connection — Quality Businesses Make DCF Easier

Consider Titan Biotech (BSE: 524717), currently trading at ₹504 per share with a market cap of approximately ₹2,082 crore. The company has an ROCE of 16.9% and ROE of 15.0%, with a book value of ₹40.3 per share (face value ₹2). These are the hallmarks of a quality business — strong returns on capital, consistent growth, and a competitive position in the biotech and life sciences space.

Quality companies like Titan Biotech make DCF analysis more reliable because their cash flows are more predictable, their competitive advantages provide a margin of error in your growth projections, and their management has demonstrated the ability to deploy capital at high returns. When you find a business with 16.9% ROCE that has been compounding steadily, your DCF assumptions rest on a much firmer foundation than when analyzing a company with volatile, unpredictable cash flows.

This is precisely why we emphasize quality stock picking over F&O gambling. According to SEBI’s own study, 9 out of 10 individual traders in the F&O segment incurred net losses. Instead of gambling on short-term price movements, use DCF to identify what a quality business is truly worth and buy it with a margin of safety.

Practical DCF Toolkit for Indian Investors

Here is your step-by-step DCF checklist:

Step 1: Go to Screener.in and pull up the company’s 10-year financial history. Note revenue growth CAGR, operating profit margins, and capital expenditure trends.

Step 2: Calculate Free Cash Flow for the last 5 years: Operating Cash Flow minus Capex. Check for consistency. If FCF swings wildly, use the 5-year average as your base.

Step 3: Estimate a conservative growth rate. Use the lower of: (a) the company’s 5-year FCF CAGR, or (b) the industry’s expected growth rate. Apply an additional haircut of 2–3% for safety.

Step 4: Set your discount rate at 12–15% depending on the company’s risk profile. Small-caps with less predictability deserve higher rates (14–15%). Large, stable compounders can justify 12–13%.

Step 5: Project FCF for 10 years, discount each year back, add terminal value, and divide by shares outstanding.

Step 6: Run a sensitivity table with 3 growth scenarios and 3 discount rate scenarios (9 combinations). Only buy if the stock is undervalued in at least 6 of 9 scenarios.

Step 7: Demand a 25–30% margin of safety below your base-case intrinsic value before buying.

DCF and the Current Market Environment

With markets jittery and geopolitical tensions (the Sensex dropped ~500 points today on Iran-related concerns), DCF becomes even more valuable. When everyone is panicking, DCF gives you an anchor. If you have calculated that a quality company is worth ₹500 per share and the market offers it at ₹350 during a panic, you know exactly what to do — buy more, not sell in fear.

Conversely, during bull market euphoria, DCF prevents you from overpaying. When the crowd pushes a stock to ₹800 but your DCF says it’s worth ₹500, you know to be patient and wait for a better entry point.

This is the essence of value investing — using rational analysis (like DCF) to make decisions that are independent of market emotion. And this discipline, practiced consistently over decades, is how long-term wealth is built in Indian markets.

Continue Your Value Investing Education

DCF is just one tool in the value investor’s arsenal. To build a complete foundation, explore our free Complete Value Investing Course on YouTube: Watch the Full Course Here.

Remember: the goal is not to get a precise DCF number — it is to develop a framework for thinking about what businesses are worth. As Buffett says, “It is better to be approximately right than precisely wrong.”

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}