The Sunk Cost Fallacy: Why Indian Investors Keep Averaging Down on Failing Stocks — The Behavioral Trap That Costs Retail Investors Billions and How to Break Free

Discounted Cash Flow (DCF) for Beginners: The Gold Standard Valuation Method That Tells You What Any Stock Is TRULY Worth — A Complete Step-by-Step Guide for Indian Investors

April 3, 2026

Overconfidence Bias: Why Indian Investors Overestimate Their Stock-Picking Skills — And How This Silent Bias Is Destroying Your Portfolio Returns

April 3, 2026

April 3, 2026

(Friday)

Imagine you bought shares of a company at ₹200. The stock falls to ₹150. You’re worried, but instead of re-evaluating the business, you tell yourself: “I’ve already put in so much money. Let me average down and bring my cost to ₹175.” The stock falls to ₹100. Then ₹60. Then ₹30.

At every step, you kept buying — not because the business was improving, but because you couldn’t accept that the money already invested was gone. This is the Sunk Cost Fallacy, and it is one of the most quietly devastating behavioral traps in investing.

According to a landmark SEBI study, 91% of individual traders in the equity Futures & Options segment incurred net losses. Even more alarming? More than 75% of those loss-making traders continued trading despite incurring losses for two or more consecutive years. That’s not bad luck — that’s behavioral psychology at work, destroying wealth in slow motion.

What Is the Sunk Cost Fallacy?

A sunk cost is any cost that has already been incurred and cannot be recovered. In investing, your purchase price is a sunk cost the moment you buy a stock. That money is spent. Whether the stock goes up or down from here, your original investment does not change — only your future decisions do.

The Sunk Cost Fallacy occurs when investors let past, irrecoverable investments influence future decisions — even when those future decisions no longer make rational sense. Instead of asking “Is this company worth investing more money in TODAY?”, the sunk-cost-trapped investor asks “How can I avoid locking in this loss?”

These are fundamentally different questions. The second one leads to catastrophically bad decisions.

How the Sunk Cost Fallacy Destroys Indian Retail Investor Portfolios

Consider the data: Net losses of individual traders in India widened by 41% to ₹1.05 lakh crore (approximately $12.5 billion) in FY25 alone. A large portion of these losses can be attributed directly to behavioral errors — with the sunk cost fallacy being the most insidious of all.

Here is how the trap works in the Indian equity markets:

1. Averaging Down on Fundamentally Broken Businesses

An investor buys a small-cap company that seemed attractive at ₹80. The company’s quarterly results disappoint — revenues stagnate, promoter holding falls, and pledged shares increase. The stock drops to ₹50. A rational investor would re-examine the thesis. But the sunk cost investor says: “At ₹50, I’m getting it at a 37% discount to what I paid!”

The critical question they fail to ask: “Would I buy this company TODAY if I had never owned it before?”

If the honest answer is no — then averaging down is throwing good money after bad.

2. Holding Indefinitely Because of a High Purchase Price

One of the most common phrases heard from trapped Indian retail investors: “Main tab hi beechunga jab mujhe mera paisa wapas milega” (I’ll only sell when I get my money back). This is the sunk cost fallacy in its purest form. The market has no memory of what you paid. The stock does not “owe” you a recovery.

3. Refusing to Redeploy Capital to Better Opportunities

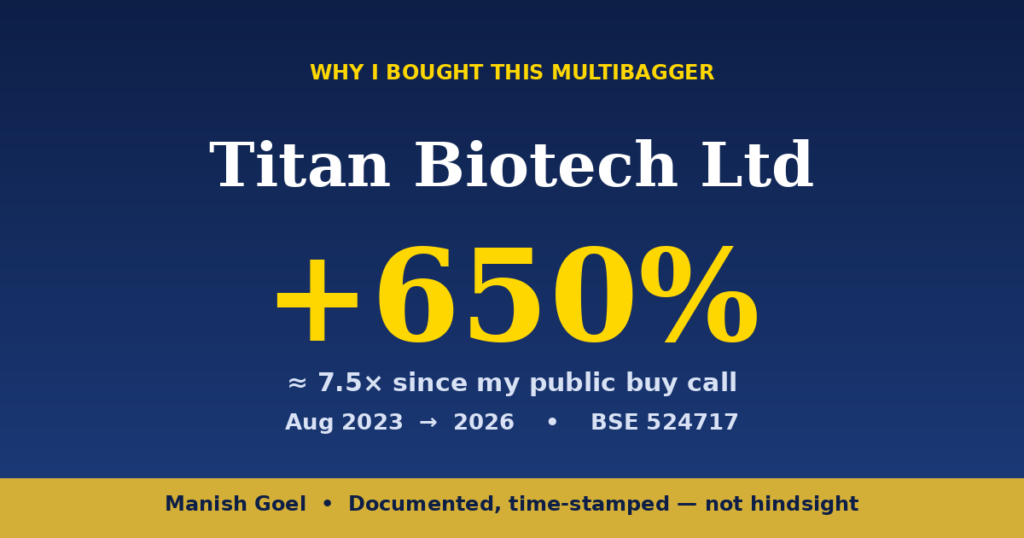

While you’re waiting for your ₹100 stock to come back from ₹40, a genuinely excellent business might be available at a compelling valuation. A stock like Titan Biotech — currently trading at ₹504 with a Market Cap of ₹2,082 Crore, consistent ROCE of 16.9%, and ROE of 15.0% — represents the kind of quality compound that rewards patient ownership. But sunk-cost-trapped investors miss such opportunities because their capital is locked in hope, not fundamentals.

The Psychological Engine Behind the Trap

Why does the sunk cost fallacy affect even intelligent people? The answer lies in two deeply human psychological forces:

Loss Aversion (Daniel Kahneman)

Nobel laureate Daniel Kahneman’s research showed that losses feel approximately twice as painful as equivalent gains feel pleasurable. This means a ₹50,000 loss feels about as bad as a ₹1,00,000 gain feels good. To avoid the psychological pain of “locking in” a loss by selling, investors irrationally continue to hold (or buy more of) a losing position.

Consistency Bias

Human beings have an innate desire to appear consistent — to themselves and to others. Once you’ve told your family, your friends, or your WhatsApp group that a particular stock is a “multibagger,” admitting you were wrong becomes a threat to your self-image. So you double down instead of reversing course.

The Classic Indian Sunk Cost Trap: Averaging Down in Broken Companies

Let’s examine a pattern that repeats itself across thousands of Indian retail portfolios every year:

Step 1: Investor buys a “story” stock at ₹200 based on tips or social media buzz.

Step 2: Stock falls to ₹140 (-30%). Investor averages down, brings cost to ₹170.

Step 3: Quarterly results disappoint. Promoter sells stake. Stock falls to ₹90.

Step 4: Investor averages down again, desperate to “recover cost.”

Step 5: Company announces debt default. Stock hits ₹20.

Step 6: Total loss: 88% of invested capital. All of it driven by sunk cost reasoning.

The bitter irony? At every step, the investor’s rational mind was sending warning signals — declining fundamentals, promoter exits, worsening balance sheet. But the sunk cost fallacy drowned out every rational signal with one loud emotional message: “I can’t sell at a loss.”

Titan Biotech: What a REAL Long-Term Investment Looks Like

Compare the above spiral to how a disciplined value investor approaches a quality business like Titan Biotech (BSE: 524717). As of today (April 3, 2026), Titan Biotech trades at:

- Current Price: ₹504

- Market Cap: ₹2,082 Crore

- 52-Week High / Low: ₹504 / ₹74.7 (post-split adjusted)

- P/E: 76.6

- Book Value: ₹40.3 per share

- ROCE: 16.9%

- ROE: 15.0%

- EPS (TTM): ₹6.59

A value investor who holds Titan Biotech does NOT hold it because of sunk costs. They hold it because the business fundamentals justify continued ownership. Every time they review the company, they ask: “Would I buy this today?” If the answer remains yes based on the quality of the business — not the purchase price — then holding is a rational decision.

That is the exact opposite of the sunk cost fallacy.

The Antidote: The “Fresh Eyes” Test

Warren Buffett and Charlie Munger famously practice what can be called the “Fresh Eyes” test: For every stock in your portfolio, imagine you do NOT own it. You have never bought it. Looking at the company RIGHT NOW, with fresh capital — would you buy it?

If yes: Your case for holding is rational. It’s based on the current merit of the business.

If no: You are likely holding for sunk cost reasons. And that is a trap.

This single mental exercise, applied rigorously once every quarter, can save Indian retail investors from billions in unnecessary losses.

3 Rules to Avoid the Sunk Cost Fallacy

Rule 1: Your Purchase Price Is Irrelevant to the Business’s Future. The market does not know or care what you paid. A company’s future cash flows, balance sheet strength, and competitive position are completely independent of your entry price. Evaluate the business on its merits today — not on what you need it to do to break even.

Rule 2: Cut Losers When the Business Thesis Breaks — Not Just When the Price Falls. Price declines happen to even the best businesses. What matters is whether the underlying THESIS is still intact. Titan Biotech falling 10% in a market correction is very different from a company’s promoter pledging shares, revenues declining, and debt rising. The former may be an opportunity; the latter is a red flag to exit.

Rule 3: Opportunity Cost Is the Real Measure. Every rupee tied up in a failing position is a rupee unavailable for a quality business. With SENSEX at 73,319 and NIFTY at 22,713 today (April 3, 2026), the Indian market offers thousands of businesses to analyze. Your frozen capital in a sunk-cost trap has a very real cost — the opportunity you’re missing.

F&O Trading and the Ultimate Sunk Cost Trap

Nowhere is the sunk cost fallacy more destructive than in Futures & Options trading. SEBI’s study confirms that 9 out of 10 individual traders in F&O lose money. The individual trader net losses in FY25 alone were ₹1.05 lakh crore. Yet the number of F&O participants in India increased from 34.8 lakh in December 2025 to 38.9 lakh in February 2026 — a 12% increase in just two months.

Why? Because every losing trader believes their losses so far were just “bad luck” — and they just need one more trade to recover. That is the sunk cost fallacy operating in its most financially destructive form.

Value investing — studying real businesses, buying quality at reasonable prices, and holding with discipline — is the antidote to this entire ecosystem of loss. We are building a community of educated, patient value investors at Multibagger Shares for exactly this reason.

Practical Application: A Quarterly Portfolio Audit

Here is a simple framework to protect yourself from the sunk cost fallacy:

Every quarter, for each stock in your portfolio, answer these questions:

1. Why did I buy this stock originally? (Write down your original thesis)

2. Is that thesis still intact today? (Yes / Partially / No)

3. If I had zero cost basis — would I buy this company right now at the current price?

4. What has changed in the business since I bought? (For better or worse)

5. Am I holding this because of the business OR because of what I paid?

If your honest answer to question 3 is “No” and your answer to question 5 is “Because of what I paid” — you are in a sunk cost trap. Acknowledge it. Exit with discipline. Redeploy the capital into quality.

Conclusion: Free Yourself From the Tyranny of Past Prices

The stock market rewards forward-thinking investors and punishes backward-looking ones. Your purchase price is history. The only question that matters in investing is: What happens NEXT in this business?

When you free yourself from the sunk cost fallacy, you stop averaging down on broken businesses. You start cutting losers early when the thesis breaks. You redeploy capital into quality compounders. And you give yourself a genuine chance at long-term wealth creation.

The Indian retail investor’s greatest enemy is not the market — it is the mental accounting that keeps them anchored to a number that only exists in their own mind.

Think like a business owner. Ask: “Would I buy more of this business today?” If no — the answer is clear, regardless of what you paid.

Want to learn more about behavioral finance and value investing? Explore our complete value investing course playlist: Value Investing Course — Multibagger Shares on YouTube

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}