Overconfidence Bias: Why Indian Investors Overestimate Their Stock-Picking Skills — And How This Silent Bias Is Destroying Your Portfolio Returns

The Sunk Cost Fallacy: Why Indian Investors Keep Averaging Down on Failing Stocks — The Behavioral Trap That Costs Retail Investors Billions and How to Break Free

April 3, 2026

Indian Market Pulse

April 3, 2026

April 3, 2026

(Friday)

The Overconfidence Trap: Why Most Indian Investors Believe They Are Above Average

Here is a question that might make you uncomfortable: Do you believe you are a better-than-average stock picker?

If you said yes — you are in very good company. Studies consistently show that 80–90% of investors rate themselves as above-average stock pickers. Mathematically, of course, this is impossible. Yet virtually every investor walking into Dalal Street, opening a Zerodha account, or scanning screeners at midnight believes they have an edge the market has not yet discovered.

This is Overconfidence Bias — one of the most pervasive, most costly, and least-discussed psychological traps in the world of investing. Today, on Good Friday 2026, with the Indian markets closed (NIFTY 50 last closed at 22,713 and SENSEX at 73,320 on April 2, 2026), let us take this quiet moment to examine a bias that may be silently eating into your long-term wealth.

What Exactly Is Overconfidence Bias?

Overconfidence Bias refers to an investor’s tendency to overestimate their own knowledge, predictive ability, and control over investment outcomes. It is not simply about being arrogant — it is a deeply wired cognitive illusion that affects even experienced professionals.

Behavioural economists have identified three distinct forms of overconfidence that investors commonly exhibit:

1. Overestimation: You believe your abilities, knowledge, or skill level is higher than it actually is. “I have studied this company thoroughly — I know it better than the market.”

2. Overplacement: You believe you are better than others. “I can pick stocks better than most retail investors, and certainly better than those overpriced fund managers.”

3. Overprecision: You are excessively certain about the accuracy of your beliefs. “This stock will definitely be ₹500 in 12 months.” No confidence interval. No admission of uncertainty. Pure certainty — which the market will eventually punish.

The SEBI Data That Every Overconfident Investor Must See

Here is the cold, hard reality. According to a landmark SEBI study on equity Futures & Options (F&O) trading in India, 9 out of 10 individual traders in the F&O segment incurred net losses. Think about that for a moment. Ninety percent of people who believed they were skilled enough to trade derivatives — intelligent people with charts, indicators, and real-time data — ended up losing money.

And yet, every single one of them started trading because they were confident they could be in the winning 10%. Every single one thought they had an edge.

This is overconfidence bias in its most financially devastating form. It is not ignorance — it is the dangerous combination of partial knowledge and excessive self-belief. The partial knowledge is enough to make you feel expert. The excessive self-belief is enough to make you take risks you cannot afford.

How Overconfidence Bias Destroys Indian Investors in Specific Ways

1. Excessive Trading and Churn

Overconfident investors trade too much. They believe they can time entries and exits better than the market. But every trade has a cost — brokerage, STT, GST, impact costs. Professor Terrance Odean, whose research is used in global MBA programmes, found that investors who traded the most earned the worst returns — not because they picked bad stocks, but because trading costs and poor timing eroded their gains systematically.

In India, this is even more pronounced. Internal data from leading discount brokers consistently shows that most active traders — those placing dozens of trades per month — systematically underperform those who trade rarely. Overconfidence drives the churn. The churn destroys the returns.

2. Under-Diversification and Concentration in “Sure Bets”

Overconfident investors tend to concentrate their portfolios in a handful of stocks they feel certain about. “This is a 100% sure thing,” they say. Every investor has had a “100% sure thing” that went down 60%. The problem is not conviction — conviction is valuable in investing. The problem is certainty without acknowledging the possibility of being wrong.

True conviction includes a margin for error. Overconfidence eliminates the margin entirely.

3. Ignoring Contrary Evidence

When an overconfident investor holds a strong view — say, “this stock will double in 6 months” — they unconsciously filter out any information that contradicts this view. Weak quarterly results become “temporary headwinds.” Promoter selling becomes “liquidity requirement.” Balance sheet deterioration becomes “investment phase.” Overconfidence fuses with confirmation bias to create a toxic cocktail that blinds investors to genuine warning signs.

4. The IPO Frenzy Trap

Every major IPO season in India reveals overconfidence at scale. Investors pile into IPOs confident they can flip for listing gains. When 200x subscription happens, investors believe their DRHP “research” (often a 5-minute scan) has revealed a future multibagger. SEBI data consistently shows that the majority of Indian IPOs deliver negative returns in the 2–5 year post-listing period. Yet the overconfident investor says, “I know which ones to pick.”

5. The “I Can Beat the Market” Illusion

Perhaps the most dangerous form of overconfidence is the belief that you can consistently outperform the market through active stock picking. Even 80% of professional mutual fund managers in India fail to beat their benchmark index over 10-year periods, as per SPIVA India Scorecard data. Yet retail investors, with less information, less time, and fewer resources, routinely believe they can do better.

This does not mean active investing is pointless. It means that overconfidence in your abilities — without honest, rigorous self-assessment — leads to accepting risks not commensurate with your actual skill level.

The Overconfidence-Proof Approach: How Quality Investors Think Differently

The antidote to overconfidence bias is not becoming paralysed by self-doubt. It is developing what Charlie Munger called “knowing the edge of your own competence” — being highly confident within your circle of knowledge, while maintaining genuine humility about what you do not know.

Here is how world-class value investors protect themselves:

Pre-Mortem Analysis: Before buying a stock, imagine it is 2 years from now and the stock has fallen 50%. Now work backwards — what went wrong? This exercise forces you to genuinely stress-test your thesis, rather than only imagining the upside scenario.

Maintain a Decision Journal: Write down WHY you are buying a stock, what your expected outcome is, and what would prove you wrong. Revisit this regularly. Overconfident investors never write anything down — because writing crystallises assumptions and makes them accountable.

Seek Out Disconfirming Evidence: Actively look for reasons your investment thesis might be wrong. Read a bearish analyst’s view. Examine the bear case seriously. Most overconfident investors only seek confirmation.

Embrace Calibrated Uncertainty: Instead of “this stock will be ₹800 in 12 months,” train yourself to say “my estimate is ₹600–₹900 within 18 months, with the primary risk being revenue slowdown.” Ranges instead of point estimates. Time horizons with buffers. Risks explicitly stated.

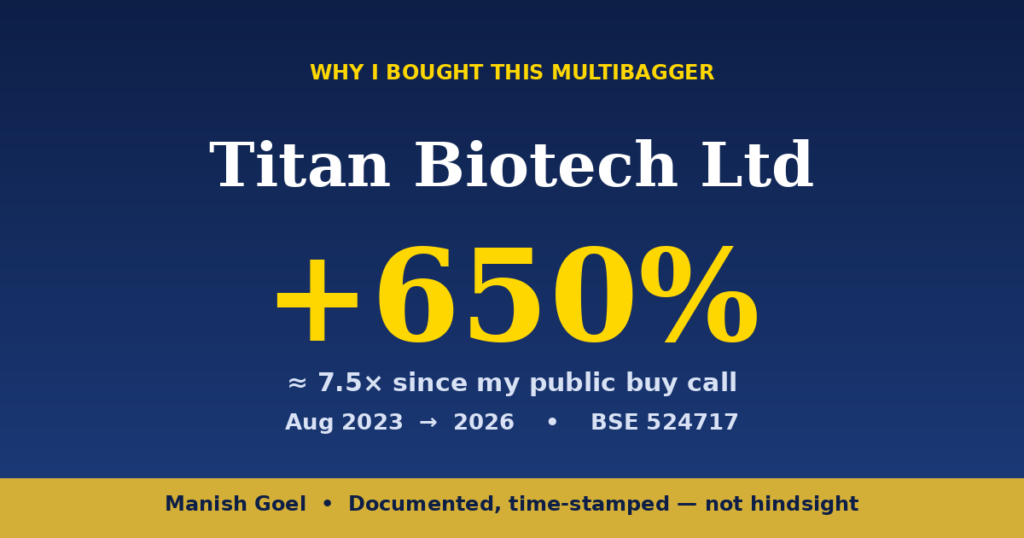

Titan Biotech: A Study in Patient, Humble Conviction

Consider Titan Biotech Ltd (BSE: 524717). As of the last trading day, April 2, 2026, Titan Biotech trades at ₹504 per share with a market capitalisation of ₹2,082 crore. The company has delivered a 431% return over the past year — extraordinary wealth creation for those who stayed invested.

But here is what the overconfident investor would have done: seen the stock at ₹150, bought a small position, and then sold it at ₹200 for a 33% gain — feeling clever. The patient investor who genuinely understood the fundamental business quality — ROCE of 16.9%, ROE of 15%, debt-free balance sheet, consistent earnings growth, and a strong niche in biological products — stayed invested through volatility and captured the real multibagger return.

The overconfident investor exited early because they believed they could predict short-term price movements. The humble, fundamentally anchored investor simply held because the business quality was evident and the long-term thesis was intact. One made 33%. The other made 431%.

This is the real cost of overconfidence — not just the money lost on bad trades, but the money not made on great businesses because you were too busy trying to be clever.

A Practical Overconfidence Checklist for Indian Investors

Before making your next investment decision, ask yourself these questions honestly:

✓ Have I actively sought out 3 credible reasons NOT to buy this stock?

✓ Have I written down my investment thesis and what would prove me wrong?

✓ Am I trading more than 4–6 times per year per stock in my portfolio?

✓ Do I have a genuine diversification strategy, or am I betting too heavily on “sure things”?

✓ Have I honestly assessed whether my past performance was skill or luck?

✓ Am I in F&O? If yes — am I in the winning 10%, or am I deceiving myself?

If you answered “no” to most of these, overconfidence may already be at work in your portfolio.

The Long-Term Wealth Equation

Warren Buffett’s greatest edge is not his intelligence — it is his intellectual honesty. He says “I don’t know” more freely than any billionaire investor alive. He acknowledges when he is wrong, publicly and with specificity. He maintains a massive cash reserve not because he lacks conviction, but because he knows the limits of his ability to predict the future.

This calibrated humility — confident where the evidence is strong, genuinely uncertain where it is not — is the hallmark of every great long-term investor. It is also the exact opposite of what overconfidence bias drives you toward.

The Indian stock market rewards patience and fundamental quality. It punishes overtrading, over-concentration, and over-certainty. As you build your multibagger portfolio, monitor not just your P&L but the accuracy of your past predictions versus what actually happened. If you have been averaging 50–60% accuracy on your conviction calls, that is not skill — that is coin-flipping with expensive transaction costs attached.

Invest in quality businesses, hold for the long term, maintain genuine humility about your timing ability, and let the fundamentals do the heavy lifting. That is the value investing formula that has created generational wealth — and it starts with honestly confronting your overconfidence.

For a deeper education in value investing fundamentals, explore our complete free course playlist: Multibagger Shares Value Investing Course on YouTube.

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}