Bonus Shares vs Stock Splits Explained: What Every Indian Investor Must Know — How Corporate Actions Create Wealth-Building Opportunities in the Indian Stock Market

How to Read a Balance Sheet Like a Pro: The Foundation Skill That Separates Successful Indian Investors from Gamblers — A Complete Guide with Real Examples

April 3, 2026

Mean Reversion in Indian Stock Markets: Why Today’s Losers Become Tomorrow’s Winners — And How Smart Value Investors Use This Timeless Principle to Find Multibaggers Before the Crowd

April 4, 2026

April 03, 2026

(Friday)

Introduction: Why Bonus Shares and Stock Splits Matter More Than You Think

If you’ve been investing in the Indian stock market for any length of time, you’ve almost certainly seen headlines like “XYZ Company announces 1:1 bonus issue” or “ABC Ltd approves 5:1 stock split.” These corporate actions send retail investors into a frenzy — stock prices surge in anticipation, Telegram groups buzz with “free shares” excitement, and trading volumes explode.

But here’s the uncomfortable truth that most Indian investors don’t understand: neither bonus shares nor stock splits change the intrinsic value of your investment by even one rupee. They are cosmetic corporate actions — like cutting a pizza into 8 slices instead of 4. You don’t get more pizza. You just get smaller slices.

Yet, paradoxically, these actions often DO create wealth — not because of the action itself, but because of what they signal about management confidence, business quality, and future growth prospects. Understanding this distinction is what separates educated value investors from the speculative crowd that chases every bonus announcement on BSE.

Today, with the Sensex closing at 73,319 and Nifty 50 at 22,713 (as of April 2, 2026 — markets are closed today for Good Friday), and with several major Indian companies announcing splits and bonuses in Q1 2026, this is the perfect time to master this critical concept.

What Are Bonus Shares? The Complete Explanation

A bonus issue (also called a capitalization issue) is when a company issues additional shares to its existing shareholders free of cost, in proportion to their existing holdings. The shares are issued out of the company’s accumulated reserves or retained earnings.

Here’s how the mechanics work. If a company announces a 1:1 bonus issue, it means for every 1 share you own, you get 1 additional share for free. If you owned 100 shares at ₹500 each (total value: ₹50,000), after the bonus you’d own 200 shares — but the price would adjust to approximately ₹250 each. Your total value? Still ₹50,000.

The accounting behind bonus shares: When a company issues bonus shares, it transfers money from its reserves (retained earnings, share premium, or general reserves) to its share capital account. This is purely a balance sheet reclassification — no cash enters or leaves the company. The company’s total equity remains exactly the same.

Think of it this way: if you have ₹1,000 in your savings account and ₹500 in your current account, and you transfer ₹200 from savings to current, your total wealth hasn’t changed. That’s essentially what a bonus issue does on a company’s balance sheet.

Real 2026 Examples of Bonus Issues in India

In March 2026 alone, we saw IRB Infrastructure Developers announce a 1:1 bonus issue, B2B Software Technologies declare a 1:2 bonus, and R M Drip and Sprinklers Systems announce a 5:7 bonus issue. Each of these announcements was met with significant short-term price appreciation — not because value was being created, but because the market interpreted these as signals of management confidence.

What Are Stock Splits? Understanding the Mechanics

A stock split is when a company divides its existing shares into multiple shares by reducing the face value per share. The total number of shares increases, but the market capitalization remains unchanged.

For example, in a 5:1 stock split, a company with a face value of ₹10 per share would reduce it to ₹2 per share. If you owned 100 shares at ₹2,000 each (total: ₹2,00,000), after the split you’d own 500 shares at approximately ₹400 each. Total value? Still ₹2,00,000.

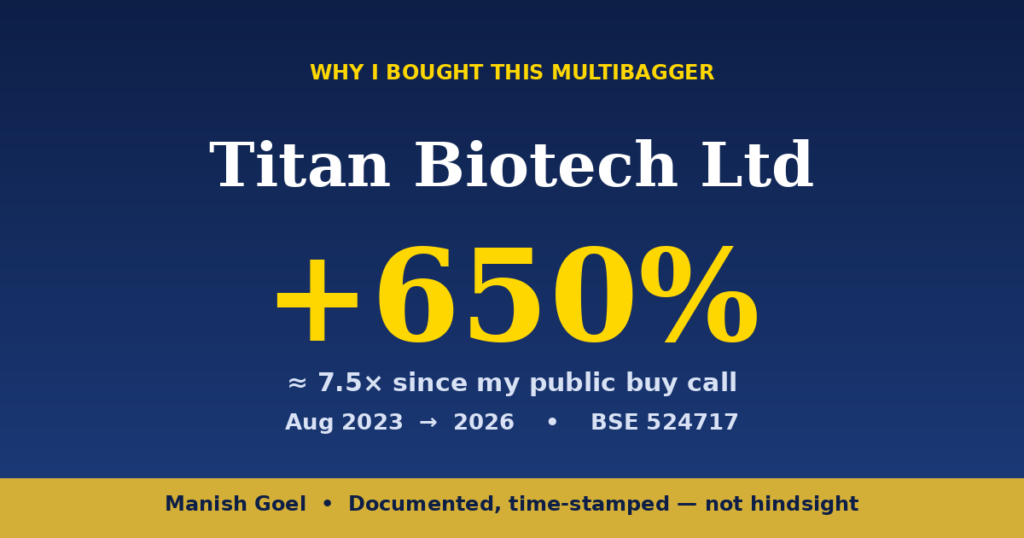

The Titan Biotech example is instructive here. Titan Biotech Ltd (BSE: 524717) — one of India’s finest quality small-cap compounders — executed a 5:1 stock split in February 2026, reducing its face value from ₹10 to ₹2. Before the split, shares were trading around ₹2,000+. After the split, the adjusted price started around ₹400. Today, Titan Biotech trades at ₹504 with a market cap of ₹2,082 Crore, ROCE of 16.9%, and ROE of 15.0%. The split didn’t change the business quality one bit — but it made the stock more accessible to retail investors who were psychologically intimidated by a ₹2,000 share price.

Another notable 2026 example: MCX (Multi Commodity Exchange) approved a 1:5 stock split, reducing face value from ₹10 to ₹2 after crossing the ₹20,000 Crore market cap milestone. Best Agrolife Ltd took an even more interesting approach — executing a 1:10 stock split followed immediately by a 1:2 bonus issue, effectively giving shareholders 20 shares for every original share held.

Bonus Shares vs Stock Splits: The 7 Critical Differences

1. Source of new shares: Bonus shares come from the company’s reserves (retained earnings are converted to share capital). Stock splits simply subdivide existing shares — no reserves are touched.

2. Face value impact: In a bonus issue, the face value per share remains the SAME. In a stock split, the face value is REDUCED proportionally. This is the single most important technical difference. If a ₹10 face value company does a 1:1 bonus, the new shares also have ₹10 face value. If the same company does a 2:1 split, the face value becomes ₹5.

3. Share capital changes: A bonus issue INCREASES the total share capital (because new shares are issued from reserves). A stock split does NOT change the total share capital — it merely subdivides existing capital into more units.

4. Reserves impact: Bonus shares reduce the company’s free reserves (since reserves are capitalized into share capital). Stock splits have ZERO impact on reserves.

5. Signal to the market: A bonus issue typically signals that the company has accumulated substantial reserves and is confident about future earnings. A stock split primarily signals that management wants to improve liquidity and make shares more accessible to retail investors.

6. SEBI regulatory requirements: Both require board approval and shareholder approval at an EGM. However, bonus issues have additional requirements under SEBI’s ICDR (Issue of Capital and Disclosure Requirements) Regulations, 2018, including specific filings about the source of reserves being capitalized.

7. Tax implications: This is crucial for Indian investors. Neither bonus shares nor stock splits trigger any capital gains tax at the time of the corporate action. You only pay tax when you eventually sell the shares. However, the cost of acquisition calculation differs — for bonus shares, the cost of the bonus shares is NIL (zero), while for stock splits, your original cost is simply divided among the new number of shares. This difference has significant implications for your tax liability when you eventually sell.

The Value Investor’s Framework: When Do These Actions Actually Create Wealth?

Now here’s where the real education begins. As value investors, we don’t get excited about cosmetic changes. We ask: “Does this corporate action tell me something about the underlying business quality?”

Here are the scenarios where bonus shares and stock splits genuinely create shareholder value:

Scenario 1: Improved Liquidity Attracts Institutional Money. When a quality stock has a very high per-share price, it becomes inaccessible to many retail investors and even some institutional investors with lot-size constraints. A stock split that brings the price into an “accessible” range (typically ₹200-₹800 for Indian small-caps) can dramatically increase trading volumes and attract new institutional investors. This increased demand CAN drive prices higher over time. Titan Biotech’s split from ~₹2,000 to ~₹400 is a textbook example — the post-split price has already risen to ₹504, a 25%+ gain, partly because more investors can now participate.

Scenario 2: Signal of Management Confidence. When a company issues bonus shares, it’s essentially saying: “We have accumulated so many profits that our reserves are overflowing, and we’re confident enough about future earnings to capitalize these reserves.” This is particularly powerful when combined with other quality signals — high ROCE (like Titan Biotech’s 16.9%), consistent revenue growth, and a clean balance sheet.

Scenario 3: Narrowing of Holding Company Discounts. In conglomerate structures common in India, stock splits of subsidiary companies can help narrow the holding company discount by making the subsidiary’s market value more transparent and liquid.

When These Actions DESTROY Value (Red Flags): Be extremely cautious when a company with declining fundamentals announces a bonus or split. Some promoters use these actions to artificially generate excitement and prop up share prices while they quietly sell their holdings. Always check: Is the promoter BUYING or SELLING around the announcement? Are revenues and profits growing? Is the company generating positive free cash flow? If the answer to these questions is “no,” the bonus or split is likely a distraction, not a wealth creator.

The SEBI Framework: What Indian Investors Must Know About Regulatory Requirements

SEBI has established clear guidelines governing both bonus issues and stock splits to protect retail investors:

For Bonus Issues: The company must have sufficient free reserves to issue bonus shares. The bonus issue must be implemented within 15 days of board approval. No bonus issue can be made if the company has defaulted on payment of interest or principal on fixed deposits, bonds, or debentures. If the company has outstanding partly-paid shares, it cannot issue bonus shares unless those shares are made fully paid-up.

For Stock Splits: The company must get approval from its board of directors and shareholders (via special resolution). The stock exchange must be notified, and a record date must be set at least 7 working days in advance. The company’s memorandum and articles of association must permit the subdivision of shares.

Key dates you must track: The announcement date (when the board approves), the record date (the cut-off date for determining eligible shareholders), and the ex-date (the first day the stock trades at the adjusted price). In India, SEBI mandates that ex-dates be announced well in advance — typically the ex-date is one day before the record date.

Tax Implications: A Deep Dive for Indian Investors

Understanding the tax treatment of these corporate actions is essential for optimizing your post-tax returns:

Bonus Shares Tax Treatment: Under the Income Tax Act, the cost of acquisition of bonus shares is considered as NIL if issued before 1st April 2001. For bonus shares issued on or after 1st April 2001, the cost is still NIL, but the period of holding starts from the date of allotment of the bonus shares (not from the date you bought the original shares). This means if you received bonus shares on January 1, 2026, you’d need to hold them until at least January 1, 2027 for them to qualify as long-term capital gains (12+ months for equity shares).

Stock Split Tax Treatment: In a stock split, your original cost of acquisition is proportionally divided among the new shares. If you bought 100 shares at ₹1,000 each (total cost: ₹1,00,000) and the stock undergoes a 5:1 split, your cost per share becomes ₹200 (₹1,00,000 ÷ 500 shares). The period of holding is calculated from your ORIGINAL purchase date — not from the split date. This is a significant advantage over bonus shares.

LTCG vs STCG: As of FY2026, long-term capital gains (holding period > 12 months) on equity shares are taxed at 12.5% above ₹1.25 lakh per annum. Short-term capital gains are taxed at 20%. The holding period calculation difference between bonus shares and stock splits can mean the difference between a 12.5% and 20% tax rate — a 7.5% difference that compounds significantly over time.

Titan Biotech: A Perfect Case Study of a Value-Creating Stock Split

Let’s examine Titan Biotech Ltd’s 5:1 stock split as a masterclass in how quality companies use corporate actions wisely.

Pre-Split Situation: Titan Biotech was trading above ₹2,000 per share with a face value of ₹10. For a small-cap company with a then market cap of around ₹1,500-1,800 Crore, this high per-share price was limiting retail participation. Many small investors on platforms like Zerodha and Groww were hesitant to invest ₹2,000+ per share in a relatively unknown small-cap biotech company.

Post-Split Reality: After the February 2026 split (face value reduced from ₹10 to ₹2), the adjusted share price dropped to around ₹400. Trading volumes surged. New retail investors who couldn’t afford the ₹2,000 price point entered the stock. Today, at ₹504, the stock has appreciated over 25% from the post-split adjusted price.

But here’s the key lesson: The split DIDN’T create the value. The underlying business quality created the value. Titan Biotech’s ROCE of 16.9%, ROE of 15.0%, consistent revenue growth in the biotech/life sciences sector, and debt-prudent balance sheet are what drive long-term wealth creation. The stock split simply removed a barrier to participation, allowing more investors to recognize and benefit from this quality.

This is the value investor’s mindset: focus on business quality FIRST, and view corporate actions as potential catalysts — never as the investment thesis itself.

A Practical Checklist: How to Evaluate Any Bonus or Split Announcement

When you see any bonus or stock split announcement on BSE/NSE, run through this 8-point checklist before making any investment decision:

1. Business Quality Check: Is the company generating consistent revenue growth, improving ROCE, and strong free cash flow? If yes, the corporate action may be a positive catalyst. If no, it may be a distraction.

2. Promoter Activity: Is the promoter increasing or decreasing their stake? Promoters who announce a bonus/split while simultaneously selling shares are sending a dangerous mixed signal.

3. Valuation Check: Is the stock reasonably valued before the announcement? If a stock with declining earnings trades at 80x P/E and announces a bonus, it’s likely a promotional tactic, not a value creator.

4. Reserve Adequacy (for bonus): Does the company have sufficient free reserves to comfortably issue the bonus shares? Check the balance sheet — reserves should be significantly larger than the proposed capitalization amount.

5. Post-Action Price Level: After the adjustment, will the stock be in a “sweet spot” for retail participation (typically ₹100-₹500 for Indian small-caps)? If the split brings the price from ₹50,000 to ₹10,000, it may not meaningfully improve retail accessibility.

6. Institutional Interest: Are mutual funds, FIIs, or DIIs already invested? Their presence before the action is a quality signal. Monitor FII/DII flows using NSDL and CDSL data.

7. Sector Tailwinds: Is the company operating in a sector with structural growth? A stock split by a company in a sunset industry is far less exciting than one in healthcare, technology, or specialty chemicals.

8. Historical Pattern: Has this company’s previous bonus/split announcements been followed by sustained gains, or did the stock price spike and crash? Pattern analysis using BSE historical data can reveal management’s track record with corporate actions.

Common Mistakes Indian Investors Make with Bonus and Split Stocks

Mistake 1: Buying AFTER the announcement hoping for “free shares.” By the time a bonus or split is announced, the expected benefit is usually already priced in. Buying at an inflated post-announcement price and holding through the ex-date often results in losses as the price adjusts downward.

Mistake 2: Confusing stock splits with value creation. Remember — a 10:1 split turns one ₹1,000 share into ten ₹100 shares. Your wealth hasn’t changed. Don’t fall for the psychological trick of “I now own 10x more shares!”

Mistake 3: Ignoring the tax implications. As we discussed, bonus shares create a NIL-cost-basis situation that can result in higher capital gains tax when you sell. Smart investors factor in the tax difference when deciding between stocks that offer bonuses vs. those that offer splits.

Mistake 4: Using bonus/split stocks for F&O trading. According to SEBI’s own study, 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses. Using the temporary volatility around corporate actions for F&O speculation is a recipe for disaster. Focus on quality stock picking and long-term value investing instead.

Conclusion: The Intelligent Investor’s Approach to Corporate Actions

Bonus shares and stock splits are among the most misunderstood corporate actions in the Indian stock market. The key takeaways for every value investor are:

First, neither action changes the intrinsic value of your investment. They are cosmetic changes to the share structure, not to business fundamentals.

Second, what matters is the underlying business quality. A stock split by a quality compounder like Titan Biotech (ROCE 16.9%, ROE 15.0%, market cap ₹2,082 Crore) is fundamentally different from a split by a fundamentally weak company trying to create artificial excitement.

Third, use the 8-point checklist before making any investment decision based on a bonus or split announcement. Focus on promoter behavior, business quality metrics, and valuation — not on the excitement of “getting more shares.”

Fourth, understand the tax implications. The cost-of-acquisition and holding-period differences between bonus shares and stock splits can meaningfully impact your post-tax returns.

The wealth in the Indian stock market is built by owning quality businesses for the long term — not by chasing corporate actions. As we always emphasize at Multibagger Shares, focus on quality investing over F&O gambling. SEBI’s data is clear: 90% of F&O traders lose money. Be in the 10% who build wealth through patient, informed value investing.

🎓 Want to learn more? Watch our complete free Value Investing Course: Value Investing Course Playlist

SEBI Disclaimer: 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to a SEBI study. F&O trading is essentially gambling. Focus on quality stock picking and long-term value investing instead.

Disclaimer: The author (Manish Goel) is a SEBI Registered Research Analyst (Registration No. INH100004775) and Multibagger Shares (Multibagger Securities Research & Advisory Pvt. Ltd.) is a SEBI Registered Investment Advisor (Registration No. INA100007736). This post is for educational purposes only and should not be construed as a buy/sell recommendation. Please do your own research and consult a qualified financial advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}