Understanding Free Cash Flow: Why It Matters More Than Profit — The One Number Every Indian Investor Must Track

The Art of Scuttlebutt: Philip Fisher’s 15-Point Checklist for Finding India’s Next Multibagger Stocks

March 26, 2026

Earnings Report Card March 2026: How BSE Ltd, Biocon

March 27, 2026

March 26, 2026

(Thursday)

Why Most Indian Investors Focus on the Wrong Number

If you ask the average Indian investor what makes a company profitable, they’ll point to the bottom line — net profit. And while profit is important, it can be misleading. Companies can report impressive profits on paper while bleeding cash in reality. The number that truly separates wealth-creating compounders from value-destroying businesses is Free Cash Flow (FCF).

As of March 25, 2026, with the Sensex at 75,273 and Nifty at 23,306 — and markets having corrected nearly 9% this month amid geopolitical tensions and ₹11.37 billion in FII outflows — understanding FCF has never been more critical. In times of market stress, companies with strong free cash flow are the ones that survive, thrive, and reward patient investors.

What Exactly Is Free Cash Flow?

Free Cash Flow is simply the cash a company generates from its operations after accounting for capital expenditures (money spent on maintaining or expanding its assets). The formula is straightforward:

Free Cash Flow = Operating Cash Flow − Capital Expenditure

Think of it this way: if a chai stall earns ₹50,000 per month in revenue and spends ₹30,000 on ingredients, rent, and labor (operating costs), and ₹5,000 on a new kettle and cups (capital expenditure), the free cash flow is ₹15,000. That’s the real money the owner can take home, reinvest, or save for a rainy day.

Why Free Cash Flow Matters More Than Net Profit

1. Profit Can Be Manipulated — Cash Cannot

Accounting profits are subject to assumptions about depreciation, amortization, revenue recognition, and dozens of other accounting policies. A clever CFO can make profits appear higher or lower depending on the narrative they want to present. But cash flow is brutally honest — either the money is in the bank, or it isn’t.

SEBI’s own studies have shown that many Indian companies that reported consistent profits on paper were actually destroying shareholder value because their cash flows told a completely different story. This is especially common in sectors like real estate, infrastructure, and capital goods where working capital cycles are long.

2. FCF Reveals True Business Quality

A company that consistently generates positive and growing free cash flow is demonstrating something powerful: its business model actually works. It’s not just booking accounting entries — it’s collecting real cash from real customers faster than it’s spending it.

Consider the best wealth creators in India’s stock market history — companies like Asian Paints, HDFC Bank, Bajaj Finance, and TCS. What do they all have in common? Consistently strong free cash flow generation, year after year, decade after decade. This is the hallmark of a true quality compounder.

3. FCF Funds Growth Without Dilution

Companies with strong FCF can fund their own growth — they don’t need to constantly raise money through equity dilution (issuing new shares) or take on excessive debt. This is crucial for minority shareholders because every time a company issues new shares, your ownership percentage shrinks.

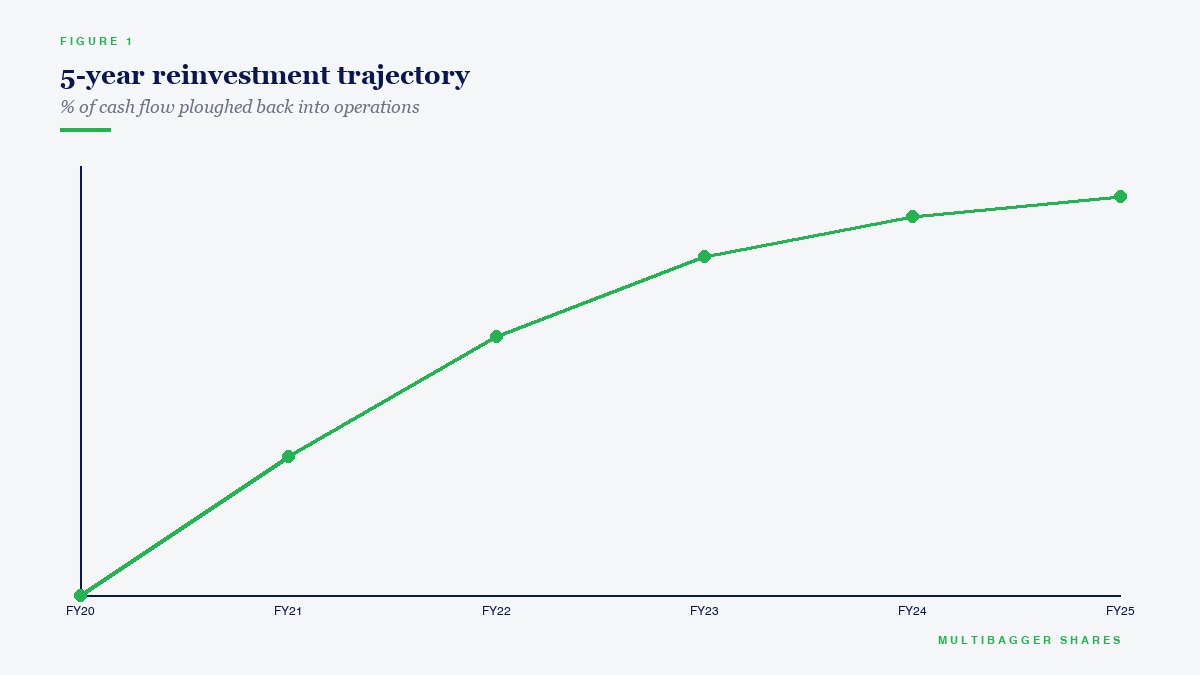

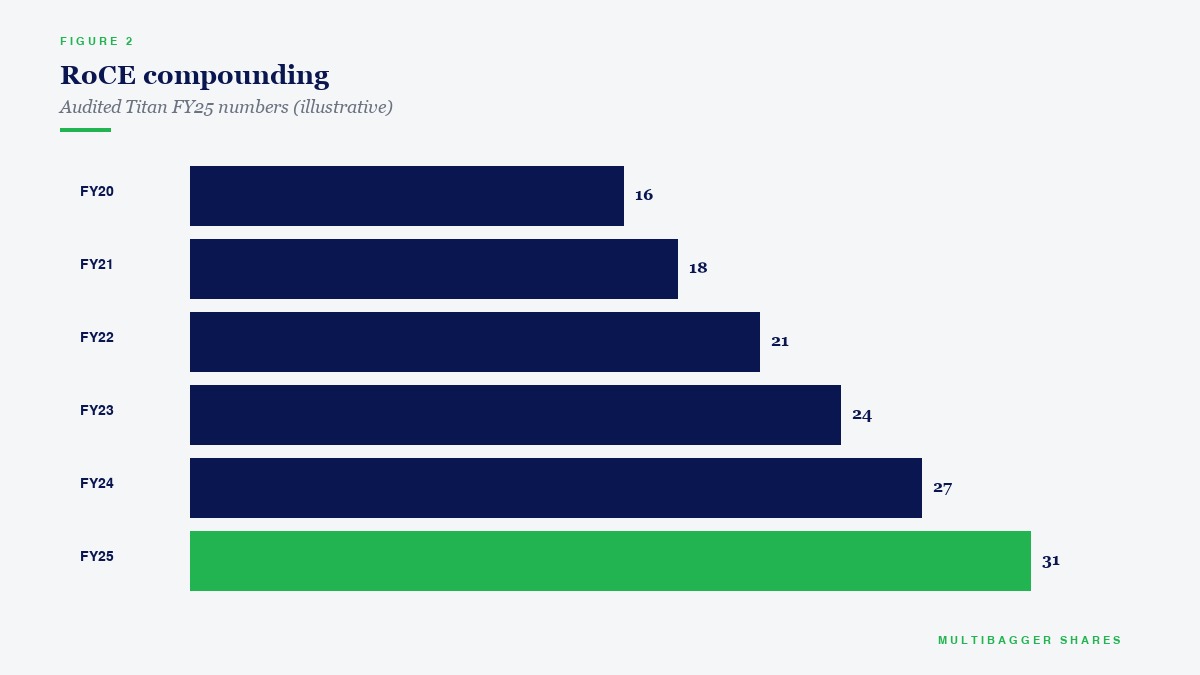

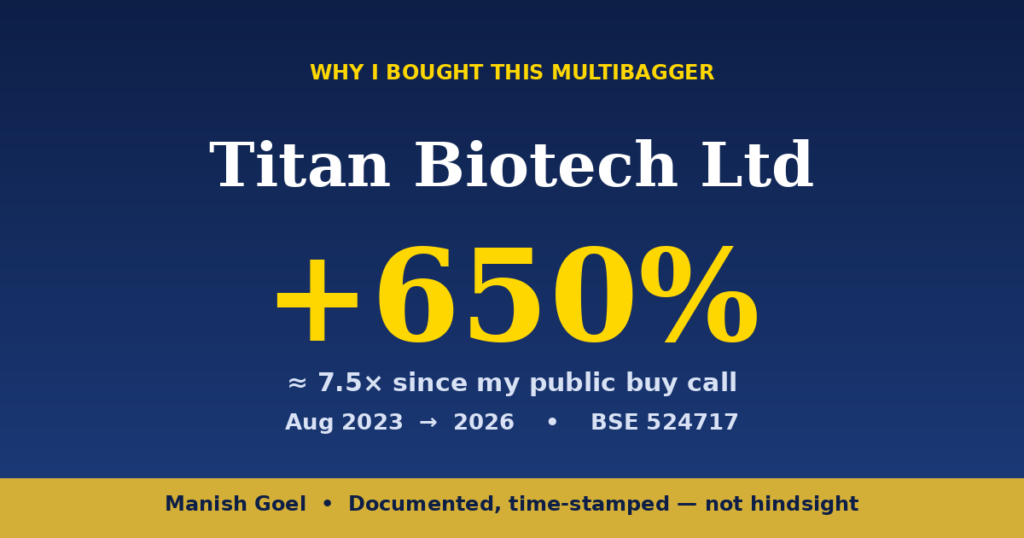

Quality companies like Titan Biotech Ltd (BSE: 524717), currently trading around ₹369 with a market cap of approximately ₹1,523 crore and a remarkable 326% return over the past year, demonstrate how businesses with strong fundamentals and capital efficiency can deliver extraordinary returns. When a company generates enough cash internally to fund its growth, the compounding effect on shareholder wealth is magnified enormously.

The Free Cash Flow Framework: How to Evaluate Indian Stocks

Step 1: Check FCF Consistency

Look at the last 5-10 years of free cash flow data. A quality compounder should have positive FCF in at least 7-8 out of 10 years. Occasional negative FCF is acceptable if it’s due to a major expansion, but chronic negative FCF despite reported profits is a red flag.

Step 2: Calculate FCF Yield

FCF Yield = Free Cash Flow per Share ÷ Current Share Price × 100

An FCF yield above 4-5% generally indicates good value. Compare this with the 10-year government bond yield (currently around 6.8-7%) as a benchmark. If a high-quality company offers an FCF yield close to or above the bond yield, you may be looking at an excellent long-term investment opportunity.

Step 3: Analyze FCF-to-Net Profit Ratio

This is a powerful quality check. Divide free cash flow by net profit. For a high-quality business, this ratio should be close to 1.0 or higher over time. If a company consistently reports profits of ₹100 crore but generates only ₹30 crore in FCF, something is wrong — the profits aren’t converting to cash.

Step 4: Watch for FCF Growth Rate

The best investments are companies where FCF is growing faster than revenue and profits. This indicates improving capital efficiency and operating leverage — the hallmarks of a compounding machine. According to Marcellus Investment Managers, companies with 25% free cash flow CAGR tend to deliver approximately 25% share price compounding over time.

Red Flags: When Free Cash Flow Tells You to Stay Away

Chronic negative FCF with positive profits: This is the classic sign of a value trap. The company is “profitable” on paper but consuming cash. Many infrastructure and real estate companies in India have this pattern — they report profits but their cash flows are perpetually negative due to ballooning receivables and inventory.

Declining FCF despite revenue growth: When a company is growing its topline but FCF is shrinking, it usually means the growth is coming at the cost of deteriorating cash conversion. This is unsustainable.

High capex-to-revenue ratio without corresponding FCF improvement: Some companies keep investing heavily but never generate adequate returns on that investment. They’re essentially running on a treadmill — always spending but never building real wealth.

The Deadly Alternative: Why F&O Trading Destroys Wealth

While patient investors who understand metrics like free cash flow build lasting wealth, a staggering number of Indian investors are destroying their capital in Futures & Options (F&O) trading. SEBI’s landmark study revealed that approximately 90% of individual F&O traders lose money, with the average loss being several lakhs per year.

Think about the irony: while quality companies are quietly generating crores in free cash flow every quarter, gamblers in the F&O market are hemorrhaging their hard-earned savings chasing quick profits. The stock market is designed to transfer money from the impatient to the patient — and understanding fundamentals like FCF is how you position yourself on the right side of that transfer.

Instead of gambling with options and futures, invest that same capital in businesses with proven FCF generation and hold for the long term. The compounding will do the heavy lifting.

Building Your FCF-Focused Watchlist

Here’s a practical approach for Indian investors:

- Screen on Screener.in: Use the free cash flow screen to find companies with consistently positive FCF over 5+ years, combined with high ROCE (Return on Capital Employed above 15%).

- Cross-check with debt levels: Prefer companies with low or zero debt. A debt-free company with strong FCF is a compounding machine. As we discussed in our earlier post on debt-free companies, zero debt is the ultimate superpower.

- Verify management quality: Check if the management is allocating FCF wisely — through dividends, buybacks, or high-return reinvestment — rather than empire-building through value-destroying acquisitions.

- Be patient during corrections: Market corrections like the current 9% decline in March 2026 are the best times to buy FCF-rich companies at a discount. When FIIs sell indiscriminately, they often sell the best companies along with the worst.

The Bottom Line: Cash Is King, Always

In a market environment where geopolitical tensions, FII outflows, and rupee depreciation dominate headlines, it’s easy to get distracted by noise. But the fundamental truth of investing remains unchanged: companies that generate abundant free cash flow will create wealth for their shareholders over time, regardless of short-term market movements.

Warren Buffett said it best: “Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.” Not earnings. Not revenue. Cash.

Focus on free cash flow. Invest in quality compounders. Avoid F&O gambling. Hold for the long term. This is the proven path to building generational wealth in India’s stock market.

Want to learn the complete framework for identifying multibagger stocks? Watch our free value investing course: Value Investing Masterclass on YouTube

Disclaimer: This article is for educational purposes only and does not constitute investment advice. The author, Manish Goel, may hold positions in stocks mentioned. Titan Biotech Ltd is referenced as an educational example of quality compounding — always conduct your own research or consult a SEBI-registered investment advisor before making investment decisions. Stock market investments are subject to market risks. Past performance is not indicative of future results. The mention of SEBI data on F&O losses is based on publicly available regulatory research.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}

{kind=link}