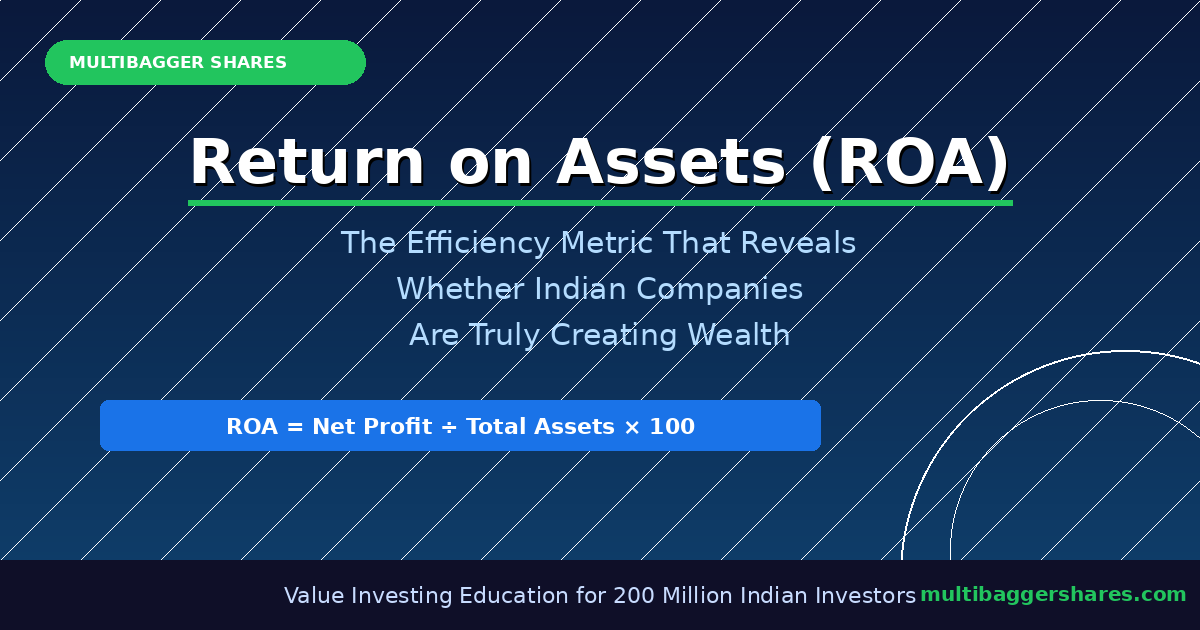

Return on Assets (ROA): The Underrated Efficiency Metric That Reveals Whether Indian Companies Are Truly Creating Wealth — A Complete Guide for Smart Investors

The Narrative Fallacy in Stock Analysis: Why Indian Investors Fall for Compelling Stories Instead of Hard Numbers — And How This Bias Destroys Wealth While You Think You’re Being Smart

March 29, 2026Mohnish Pabrai’s Dhandho Framework: The Low-Risk, High-Return Value Investing Method That Turned a Gujarati Business Philosophy Into Billions — A Complete Guide for Indian Investors

March 29, 2026

March 29, 2026

(Sunday)

When most Indian investors evaluate a stock, they focus on profit margins or return on equity. But there is one metric that cuts even deeper — one that reveals the fundamental efficiency of a business in generating profits from everything it owns. That metric is Return on Assets (ROA), and once you understand it, you will never look at a company’s balance sheet the same way again.

With the BSE Sensex at 73,558 and Nifty 50 at 22,769 (as of March 27, 2026), markets are facing pressure from global headwinds — Goldman Sachs has lowered India’s GDP growth forecast and downgraded Indian equities. In this environment of uncertainty, identifying genuinely efficient, high-quality companies becomes more important than ever. ROA is your flashlight in the dark.

What Is Return on Assets (ROA)?

Return on Assets measures how much net profit a company generates for every rupee of total assets it employs. It is one of the most honest efficiency metrics in finance because it cannot be gamed by financial engineering or leverage.

📐 The Formula

ROA = (Net Profit ÷ Total Assets) × 100

Example: A company earns ₹50 crore net profit on ₹500 crore total assets → ROA = 10%

A company with an ROA of 15% is generating ₹15 of profit for every ₹100 of assets it owns — machines, inventory, receivables, buildings, cash, everything. A company with ROA of 3% is grinding very hard for very little reward.

ROA vs ROE — Why Both Matter

Many investors are familiar with Return on Equity (ROE) — we covered this topic in detail recently. ROE measures returns on shareholder equity. But ROE has a dangerous blind spot: it can be inflated by debt. A company can borrow heavily, inflate its asset base, and boost ROE mechanically — without genuinely becoming more efficient.

ROA bypasses this problem entirely. It uses total assets — both equity and debt-funded — in the denominator. This means:

- A company with high ROE but low ROA is likely using excessive leverage — a red flag

- A company with high ROA and high ROE is a genuine wealth-creation machine

- When ROA and ROE are both high and rising over 5 years — that is your multibagger signal

⚠️ The Leverage Trap

Imagine Company A earns ₹10 crore profit on equity of ₹50 crore but total assets of ₹200 crore. ROE = 20%. ROA = 5%. The high ROE is borrowed, not earned. Now compare Company B: ₹10 crore profit on equity of ₹80 crore, total assets of ₹100 crore. ROE = 12.5%. ROA = 10%. Company B is actually the better business — less leveraged, more genuinely efficient.

What Is a Good ROA? Industry Benchmarks

ROA varies enormously by industry, and comparing a bank’s ROA to a software company’s ROA would be meaningless. Here are practical Indian market benchmarks:

| Sector | Good ROA | Excellent ROA |

|---|---|---|

| Banking / NBFC | 1–1.5% | >1.5% |

| Manufacturing / Industrials | 5–8% | >10% |

| FMCG / Consumer | 10–15% | >20% |

| IT / Software Services | 15–20% | >25% |

| Pharma / Biotech | 8–12% | >15% |

| Specialty Chemicals | 8–12% | >15% |

The key rule: always compare ROA within the same sector. A bank with 1.8% ROA is extraordinary. A software company with 1.8% ROA would be a disaster.

The 5-Year ROA Trend: Your Most Powerful Screening Tool

A single year’s ROA tells you little. What you want to see is the 5-year ROA trend. This is where the real story lives:

- Rising ROA trend = Company becoming more efficient, pricing power strengthening, moat widening

- Stable high ROA = Established moat, consistent execution, reliable compounder

- Falling ROA trend = Competition intensifying, cost inflation eating margins, or over-investment in low-return assets

- Sudden ROA spike = Could be a one-time event — investigate before celebrating

Screener.in is your best friend here. Look up any company, go to the 10-year data table, and track how ROA has moved over time. A company that has consistently maintained ROA above 12% for 7–10 years is genuinely rare and valuable.

Real Indian Examples: ROA in Action

Asian Paints — The Gold Standard

Asian Paints has consistently delivered ROA in the range of 20–28% over the past decade. For a manufacturing company that owns factories, inventory, and distribution infrastructure, this is phenomenal. Every rupee of assets deployed generates exceptional profits — the hallmark of a true moat business. This is why Asian Paints has been a 100x+ compounder over the long term.

TCS / Infosys — Asset-Light ROA Champions

India’s IT giants maintain ROA of 20–35% because software services are asset-light. They don’t need heavy machinery or large inventories. This structural advantage means every rupee of asset generates enormous profits. When you see an asset-light company with high ROA, you are looking at a business with an intrinsic structural moat.

A Cautionary Tale: Heavily Leveraged Infrastructure Companies

Several Indian infrastructure companies showed impressive ROE in the 2000s, attracting retail investors. But their ROA was consistently below 3–4% while they piled on debt. When credit cycles turned, these companies were destroyed. ROA would have warned you years earlier.

Titan Biotech: A Quality Pharma-Biotech Business

With Titan Biotech (BSE: 524717) trading around ₹368–370 per share (having surged over 326% in the past year and reaching a 52-week high of ₹400), the company exemplifies the pharma-biotech segment that sophisticated ROA-focused investors seek.

Titan Biotech operates in the high-value segment of biological products, bacteriological culture media, and specialty nutritional products — an area where asset utilisation efficiency matters enormously. Quality pharma-biotech companies that maintain strong ROA trends — consistent, improving efficiency in deploying their laboratory equipment, R&D assets, and working capital — are the kind of businesses that can create long-term, sustainable wealth for patient investors.

🌱 The Quality Investing Principle

Focus on businesses with improving ROA trends over 5 years, debt-free or low-debt balance sheets, and strong pricing power in their niche. This combination — not F&O gambling — is how real wealth is built in Indian markets. SEBI data shows 90% of F&O traders lose money. Long-term quality investing wins every time.

How to Use ROA in Your Stock Research: A Step-by-Step Framework

Step 1 — Gather 5-Year ROA Data

Go to Screener.in, look up the company, and note ROA for each of the last 5–7 years from the “Key Metrics” or annual data tables.

Step 2 — Compare to Industry Peers

ROA is only meaningful in context. Note the ROA of the top 3–4 sector peers. Is your company above or below industry average? Is the gap widening or narrowing?

Step 3 — Check the ROE-ROA Gap

Calculate the ratio of ROE to ROA. If ROE is 20% and ROA is 4%, the company is using 5x financial leverage. This is a risk flag. Ideal companies have ROE/ROA ratios of 1.5x or less (indicating modest leverage).

Step 4 — Look for the Inflection Point

One of the most powerful signals: a company with average ROA that suddenly starts improving. This often signals a new product launch, capacity utilisation reaching an inflection point, or management making better capital allocation decisions. These inflection points are where multibaggers are born.

Step 5 — Combine with Other Quality Metrics

ROA works best as part of a quality screening framework. Combine it with: Operating Cash Flow (positive and growing), Debt-to-Equity (preferably below 0.5x), and Revenue growth consistency. A company ticking all these boxes is a high-quality business worth deep analysis.

ROA Red Flags: When to Stay Away

- Chronically declining ROA over 3+ years despite growing revenues — suggests cost structure is deteriorating

- ROA much lower than industry average for 5+ years with no clear turnaround catalyst

- Large goodwill or intangible assets inflating the denominator — ROA looks low but may be distorted; check tangible ROA separately

- Asset-heavy businesses with ROA below 5% — the returns don’t justify the capital deployed

- Sudden asset write-offs that boost ROA artificially — always check the notes to accounts

Advanced Application: DuPont Decomposition of ROA

For those who want to go deeper, ROA can be decomposed using the DuPont framework:

📊 DuPont Decomposition

ROA = Net Profit Margin × Asset Turnover

Where Asset Turnover = Revenue ÷ Total Assets

This decomposition is powerful because it tells you why a company has its ROA:

- High margin + high turnover = Exceptional business (rare and valuable)

- High margin + low turnover = Premium niche business (luxury goods, specialty chemicals) — sustainable if moat is real

- Low margin + high turnover = Volume business (retail, distribution) — depends on volume consistency

- Low margin + low turnover = Avoid. Capital destroyer.

Asian Paints falls in the high-margin/decent-turnover bucket. Retailers like D-Mart operate on low margins but exceptionally high asset turnover. Both can generate strong ROA — just through different business models.

The Value Investing Edge

In a market where 90% of F&O traders lose money (as documented by SEBI), the patient investor who screens for high and improving ROA, holds quality businesses for 5–10 years, and ignores daily price noise has an enormous statistical advantage. This is not speculation — it is the documented, repeatable approach of India’s greatest wealth creators.

When you find a company with:

- ROA consistently above 12–15% for 5+ years

- ROA trend rising, not falling

- Debt-to-equity below 0.5x

- Operating cash flow matching or exceeding net profit

- Management with skin in the game

…you are looking at the building blocks of a potential multibagger. Your job then is to buy it at a reasonable price and have the patience to let compounding do its work.

📚 Watch our complete Value Investing Course on YouTube — completely free, designed for 200 million Indian investors.

Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. The stock market involves risk. Please consult a SEBI-registered investment advisor before making any investment decisions. Past performance is not indicative of future returns. Multibagger Shares is a value investing education platform only.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

{kind=link}

{kind=link}